$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '3051',

'magazine_issue_id' => '1024',

'magazine_category_id' => '21',

'title' => 'Riding THE BOOM',

'image' => '20210630085625_Clipboard11.jpg',

'short_content' => 'Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.',

'content' => '<p><strong>--BY SAGAR GHIMIRE</strong></p>

<p>There is not a single sector in the economy in the last one and a half years that has not borne the brunt of the Covid-19 pandemic.</p>

<p>Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.</p>

<p>Businesses and industries either closed down or operated below their capacity as authorities imposed a nationwide lockdown for four months (between March 24 and July 21 in 2020) last year to contain the spread of the virus. The latest prohibitory orders, which were imposed in April, continue to be in place in many parts of the country to combat the deadly second wave of Covid-19.</p>

<p>As almost all sectors including tourism, retail businesses, manufacturing, foreign trade, construction, education and transportation were hit by the pandemic, the economic growth of the country for the first time in many years observed a contraction of two percent in the last fiscal year (2020/21), according to the Central Bureau of Statistics (CBS).</p>

<p>Amid this gloom, one sector of the economy, however, stood out as an exception: the stock market.</p>

<p>Prices of stocks of listed companies in Nepal Stock Exchange (Nepse), the only stock exchange in the country, have been on an upward trend for last one and a half years. In line with the rise in the Nepse benchmark index which has been recording fresh highs in recent days, most of the stocks listed in the market have seen huge gains in their values during this boom.</p>

<p>The Nepse benchmark index climbed up to an all-time-high of 3,025.83 points on June 14. There was also a surge in both daily transactions and turnover in the stock market. Market capitalization—the total value of all listed companies based on their trading price—also reached Rs 4,216 billion on June 14, which means the total value of the stock market is equal to the size of the country’s overall economy as measured through Gross Domestic Product (GDP). Nepal’s projected GDP in the current fiscal year (2020/21) stands at Rs 4,266.3 billion, according to the CBS.</p>

<p>Market analysts point to a number of factors that have fueled the stock market boom including cheaper bank interest rates, lack of alternate investment avenues for investors and entry of new investors in the market in droves. </p>

<p>While the bull run, as it is known in the stock market parlance for a continuous rise of stocks, has increased the value of the assets that investors hold in the form of securities, at least on paper, the market rally has also raised eyebrows.</p>

<p>The disconnect between the stock market and the real economy has left analysts questioning the sustainability of the rally.</p>

<p>Most of the stocks’ upward movement in the secondary market is largely detached from the performance of the companies. Even those loss-making companies with weak financial indicators have seen their share price soaring in the secondary market.</p>

<p>Ankhukhola Hydropower Company Ltd exemplifies this trend in the stock market. According to the company’s third quarterly financial results for the current fiscal year, its net worth per share is Rs 64.05 and earnings per share (EPS) is minus 13.89. The loss-making hydropower company has not even been in a position to distribute dividends to its shareholders for at least a few years. However, investors do not seem to be bothered by the company’s performance. The buying spree in the market sent the share price up to a record high of Rs 335 on June 14. </p>

<p>Though this company is still to start generating electricity and earning revenue, and the investors may be buying this company’s shares in anticipation of future profits, the current share prices of this company are much higher than that can be justified. </p>

<p>Similar is the case with many other stocks. Regardless of their performance, almost all companies listed in the Nepse have witnessed the value of their stocks soaring during the market rally. It is despite the fact that the pandemic has either dealt a heavy blow to most of the listed companies or affected their bottom line.</p>

<p>Still, investors are continuing to pour money into those stocks to propel the stock market to the peak, shrugging off concerns of ‘unjustified bullish sentiment’.</p>

<p>Analysts suggest that the performance of the economy or fundamentals of a company may not always dictate the course of the market.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard13%2829%29.jpg" style="float:right; height:428px; margin:10px; width:250px" />“Like in the current scenario of our market, it’s not the fundamentals or the course of the economy that always drives the rally. Higher valuation of stocks also reflects the bullish sentiment of investors or their future expectations from those companies and the recent policy easing that favours companies and investors. This happens also in stock markets in other countries,” says Prakash Tiwari, a stock market analyst.</p>

<p>From Dow Jones, S&P 500 and Nasdaq Composite index of the US to Nikkei 225 of Tokyo Stock Exchange to FTSE 100 of the London Stock Exchange to BSE Sensex and Nifty in India, most of the stock markets around the world surged during the pandemic.</p>

<p>“There are various factors at play,” says Tiwari. </p>

<p>One major factor is the low interest rate of banking institutions.</p>

<p>Amid a sharp decline in economic activity during the pandemic which has depressed the demand for loans, banks and financial institutions (BFIs) are slashing their interest rates. Interest rates in both saving accounts and fixed deposits have also gone down sharply. Awash with liquidity, BFIs, which were competing with each other to attract deposits until a few years ago due to shortage of lendable funds, are even reluctant to accept deposits at more than three percent on savings accounts and seven percent on one-year fixed deposits.</p>

<p>According to the Nepal Rastra Bank’s statistics, the weighted average interest rate on credit stood at 8.53 percent in mid-May compared to 12.22 percent two years ago. The weighted average interest rate on deposit also fell to 4.81 percent from 6.67 percent.</p>

<p>While the pandemic either discouraged or restricted investments in other businesses or projects for investors, the stock market, already on an upward trend, emerged as a promising avenue. Various measures introduced by the government and the NRB to ease the policies and provide relief to businesses and enterprises battered by the pandemic also supported the stock market rally.</p>

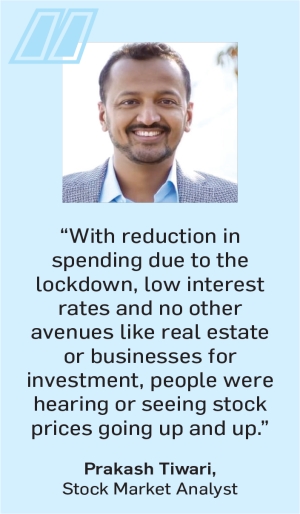

<p>“People were shut in their homes due to the lockdown or prohibitory orders. At the same time, Nepse implemented a system allowing investors to trade stocks online. With reduction in spending due to the lockdown, low interest rates and no other avenues like real estate or businesses for investment, they were hearing or seeing stock prices going up and up,” says Tiwari. “They felt like they would miss the boat if they did not immediately jump into the market. But they should be aware about financial risks in the market. It's not always bullish, but sometimes brutally bearish also.”</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard14%2845%29.jpg" style="height:462px; width:800px" /></p>

<p><strong>Stock market gold rush </strong><br />

After returning from the UK a few years ago, Shambu Dhital, 36, was planning to open a restaurant in Kathmandu from his savings. However, he gave up his business plan after the coronavirus swept across the country.</p>

<p>Disappointed with the low interest rates on fixed deposits, he decided to pour his money into some insurance and hydropower stocks on the advice of one of his friends who was ‘also making money’ in the market, he says. He claims that the value of stocks that he picked with the help of his friends has nearly doubled in the last six months. He, however, declines to divulge the details of his investment.</p>

<p>“The value of my shares has doubled. This level of gain would not have been possible if I had invested it in opening a restaurant,” says Dhital. </p>

<p>Stock brokers say that there has been a huge growth in the number of investors in recent months, particularly during the prohibitory period when Covid-19 containment measures closed the physical floors of brokerage firms for investors and trading went completely online.</p>

<p>Though there is no exact figure of stock investors in the country, online accounts created by brokerage firms give an estimate of those who were actively trading during the pandemic. </p>

<p>According to Nepse, 703,885 online accounts have been created, a majority of them in the last three months when many parts of the country including the Kathmandu Valley were closed due to prohibitory orders.</p>

<p>Adoption of technology for trading facilitated the surge of new investors.</p>

<p>Compared to the lengthy process of visiting the trading floors of brokerage firms to manually fill out forms and place buy or sell orders of shares, it all went online. Many investors, not allowed to step out of their homes due to the prohibitory orders, were now glued to their computers or mobiles to watch the movement of stock prices in the secondary market. From Facebook groups to rooms of new voice-only social media app ClubHouse, discussions were flooded with investors looking for stock market basics, tips and trends about investment.</p>

<p>However, the stock market did not start attracting the public only after the trading went online. With the implementation of the full-fledged dematerialised form of share trading system in 2016 and the facility to apply shares through Mero Share app, public offerings of various companies were already attracting an overwhelming number of investors. As most of the companies were floating their primary shares at a face value of Rs 100, which would eventually rise multifold in the secondary market, they were selling like hotcakes. The adoption of a full-fledged online system in stock trading has given an impetus to the growth of the market. Thanks to the online trading system, the share market, which was largely limited to the Kathmandu Valley, has now expanded to other parts of the country to some extent.</p>

<p>Brokers say that some Nepalis who are working abroad have also been trading in the stock market in recent days. </p>

<p>The recent volume of daily transactions and market turnover also partly reflects a significant growth in the number of investors. The daily transaction amount, number of transactions and number of traded shares have also jumped by multifold in recent months.</p>

<p>According to Nepse, the stock market recorded a daily turnover of Rs 13.94 billion from the trading of 29.52 million units of shares through 139,247 transactions per day on an average in the month of Jesth (between mid-May and mid-June) this year. In the same month two years ago, Rs 822 million worth of 2.61 million units of shares changed hands through 9,939 transactions on an average daily. On June 13, the stock market recorded the all-time-high daily turnover of Rs 19.55 billion.</p>

<p>“While the growth in the turnover is largely attributed to the surge in stock prices, the rise in the number of transactions and traded shares also show that there is a significant growth in the number of investors in the market,” says Priya Raj Regmi, former president of Stock Brokers Association of Nepal (SBAN). </p>

<p>Retail penetration not only helps expand the investors’ base but also provides more depth to the market. Nonetheless, the way these new investors are jumping into the market also has its downsides.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard16%2831%29.jpg" style="float:right; height:410px; margin:10px; width:250px" />“While the surge of new investors helps in strengthening the base of the stock market in the long-term, they are also prone to making poor investment decisions based on speculations and rumours as we can often see in their irrational behaviour in the market. A faster ride also comes with higher risk,” says Mekh Bahadur Thapa, chairman of Merchant Bankers Association of Nepal (MBAN).</p>

<p>Pointing out to a risk of an exodus of investors when there is even a slight correction in the market, he underscores the need for massive awareness and education programmes which he says will help investors make informed investment decisions and prepare them for the adverse market scenario.</p>

<p>But the growing clout of mutual funds and other bigger players in the stock market is expected to reduce the volatility in the market to some extent. This was not the case a few years ago due to their limited number and investment capacity. There are now 22 mutual fund schemes with a portfolio of over Rs 22 billion. There are also insurance companies active on share trading. Some business houses also have reportedly entered the market during the recent boom. As they make investment decisions largely based on fundamental and technical analysis, they could play a significant role in reducing market volatility, according to experts.</p>

<p>“Every market has its cycle. Nobody can completely rule out a worse scenario in the market. However, mutual funds’ number and size have gone up in recent years. They make investments based on fundamental analysis which can help stabilise the market to a certain extent during the volatility,” says Thapa. </p>

<p>Concerns over the longevity of the boom are being raised as the stock market has never witnessed such a huge growth at such a short interval of time. The previous bull run that had started in 2012had continued till 2016 with Nepse index jumping nearly six times. But this time it had increased 2.7 times within 19 months.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard15%2834%29.jpg" style="height:390px; width:800px" /></p>

<p><strong>Ending dominance of banking sector</strong><br />

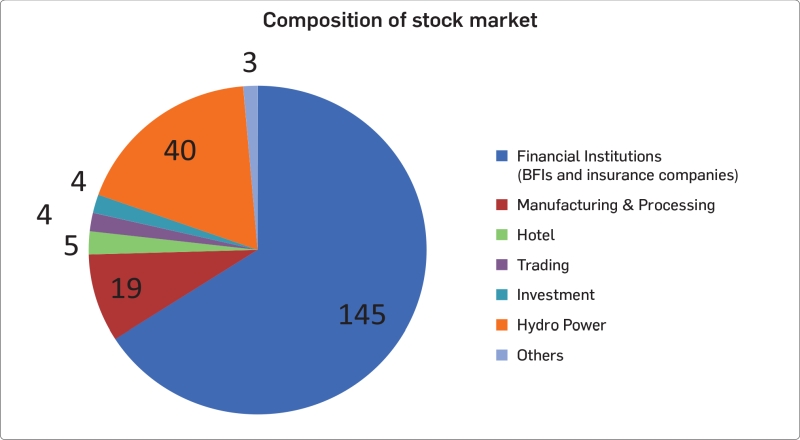

The stock market is largely dominated by banks and financial institutions. Nearly two-thirds of listed companies are banks and financial institutions (BFIs). The dominance of the banking sector has often prompted the market to move based on the decision or policy of the NRB. Investors also complain that they are facing problems diversifying their portfolio due to the low presence of non-banking scrips. The entry of real sector companies in the market is also expected to counterbalance the dominance of the banking sector. </p>

<p>Those who do not want higher exposure to banking scrips are currently left with little choice when investing in the market. Realising that the stock market has failed to represent all sectors of the economy, the government has taken some measures including the offer to provide income tax rebates to rope in companies from various sectors. </p>

<p>The government even tried to make listings mandatory for certain companies similar to banks and insurance companies.</p>

<p>The government also seems to have abandoned the plan to make it mandatory for manufacturing companies that have capital of more than Rs 1 billion to get listed in the stock market. The plan was announced in the budget speech of fiscal year 2018/19, but the government has not taken any further initiatives for this since then except that the Ministry of Finance had asked the Company Registrar’s Office to provide the list of companies that have capital more than Rs. 1 billion.</p>

<p>The majority of the newly listed companies are still from the banking or insurance sectors. In recent years, hydropower companies have also been at the forefront of public offerings. However, companies from the manufacturing, hospitality, education and other sectors have not shown much interest in the listing.</p>

<p>Except for Shivam Cement Ltd and Chandragiri Hills Ltd, all two dozen companies which were listed in Nepse in the last two years are either from the banking and insurance or hydropower sectors.</p>

<p>One of the major factors discouraging companies from making a public offering has been the share pricing system which was making it either impossible or extremely difficult for companies to sell their shares at a price higher than the face value of Rs 100.</p>

<p>While Securities Board of Nepal (Sebon) has started to allow issuing IPOs at a premium since 2016 after the enactment of Securities Registration and Issue Regulation, many companies were finding it difficult to qualify for that privilege. However, Sebon decision to introduce the book building method is expected to facilitate it though it is yet to be tested.</p>

<p>When it comes to the pricing system, Sebon was always under pressure from two extremes: the mass that always stood against ending the long-standing practice of pricing primary shares at a face value of 100 and the promoters looking for a free hand in determining the premium of their companies’ shares, according to market experts. </p>

<p>“As Sebon was caught between these two extremes, we could not have a stable policy on the pricing of shares. There was a public offering at face value. Then, we also have a policy on allowing offering shares at a premium with strict provisions,” says Mekh Bahadur Thapa, Chairman of Merchant Bankers Association of Nepal (MBAN). </p>

<p>Those companies who are financially doing well were always concerned with the pricing system of floating shares at Rs 100, according to Thapa. “Now, Sebon has introduced the book building method which is an internationally accepted practice of determining share prices based on a bidding process. This will encourage better companies to list themselves and increase the share of the non-banking sector in the stock market,” says Thapa, who is also Deputy CEO of NIBL Ace Capital.</p>

<p>Two manufacturing companies—Reliance Spinning Mills and Sarbottam Cement—are now in the process of floating their shares based on the newly introduced book building method.</p>

<p>Investors and the public also expect the initial public offering (IPO) of the first private mobile service provider Ncell in the near future. While Ncell has not officially confirmed or denied its IPO plan, the mobile service provider’s recent decision to convert into a public limited company has been interpreted as its intention to list itself on the stock market. The listing of the largest private sector mobile service provider will also help in reducing the dominance of the banking sector in the stock market.</p>

<p>“Diversity of listed companies in the market helps investors in managing market volatility. The government and Sebon should create a favourable environment for companies from various sectors for their stock listing,” says Thapa.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard20%2818%29.jpg" style="height:440px; width:800px" /></p>

<p><strong>Regulator’s roles for reforms</strong><br />

While a number of reform measures have been implemented in recent years, experts say that the government and Sebon are too slow to act on the basis of the market’s needs. It took years for the government to phase out paperless trading in the securities market that was still in place until 2014.</p>

<p>After implementing a full-fledged dematerialised system from 2016, Nepse introduced the internet-based NEPSE Online Trading System (NOTS) in 2018, paving the way for investors to carry out trading online. Eliminating the cumbersome manual process in the IPO, ‘Mero Share’ was introduced that not only allowed investors to participate in the public offering through the internet but also attracted the public to the capital market.</p>

<p>Though the stock market is still considered a laggard in terms of technological revolution, the gradual adoption of technology is making trading of securities convenient, lowering costs and expanding the reach of investors, according to experts. However, frequent technical glitches on day-to-day trading, cybersecurity vulnerabilities and lack of capacity of many investors, brokers and regulators to embrace the new system have posed a challenge and stopped the sector from taking full advantage of the technological advancements in the market. The privatisation of Nepse, which is owned by the government, is long overdue. Promises to open the stock market for non-resident Nepalis are yet to materialise.</p>

<p>According to analysts, Sebon is struggling to keep up with the market growth. Due to its weak capacity of surveillance and enforcement, it has failed to crackdown on various market anomalies including cases of insider trading, cornering and stock manipulation.</p>

<p>Sebon often faces criticisms for failing to play the regulatory role effectively as it did recently.</p>

<p>A recent decision of Sebon to list 51 companies as ‘risky’ stocks (including Ankhu Khola, the case cited above) sparked anger among investors and analysts. In its statement issued amid a stock market boom, Sebon on June 15 not only announced that it was investigating insider trading, circular trading and cornering in those 51 scrips, but also urged investors to consider its list while making investment decisions.</p>

<p>Not for the first time has Sebon weighed in with its appeal to investors to tread cautiously in the market.</p>

<p>While earlier statements used to be limited to urging investors to invest on the basis of informed decisions, Sebon this time went a step further to single out 51 scrips as ‘risky’, citing its preliminary analysis.</p>

<p>Such a ‘knee jerk reaction’ to the stock movement is unbecoming of the regulator, say analysts.</p>

<p>“The government or a regulator should become a referee to ensure that there is fair play in the market. It must not become a player itself. There are so many things that it has to prioritise including continued surveillance, investment in software and issuing brokerage licenses to new companies,” says Biswo Poudel, an economist. “Rather than reacting to the stock price movement, the regulator should focus on market reforms,” he says. </p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard18%2830%29.jpg" style="float:right; height:431px; margin:10px; width:250px" />Sebon officials, however, defend the move. “Of course, there are many things that Sebon has to do for the development of the securities market in the country. What we should not forget is that we also have a responsibility of protecting investors’ interest. So, it’s our duty to urge them to remain cautious,” says Niraj Giri, Sebon’s Executive Director and Spokesperson. “The list that we have published is based on our analysis of certain parameters and indicators. We have a duty to ask investors to become cautious while making investment decisions. We have asked them to just separate the wheat from the chaff,” says Giri.</p>

<p>But, nowhere in the world does a stock market regulator publish a list of companies saying it’s over valued based on PE ratio or net worth, say stock market analysts. For example, Amazon and other companies listed in the US stock markets have been trading at price way higher than its price to earningratio, but the US Securities and Exchange Commission (SEC) has never come up with such a list.</p>

<p>For them, the Sebon’s statement is akin to NRB publishing a list of banks terming them ‘risky’ and asking depositors to be cautious while choosing banks to park their money.</p>

<p>However, Sebon’s move did cause the market to reverse, though it seems only a temporary decline. After the release of the statement, Nepse benchmark index took a dive of over 120 points, or3.97 percent, in mere three trading days. Analysts say that the decline reflects the reaction of investors who were worried with the regulator’s perception towards the stock market rally. However, the market started showing revival on June 22, indicating that the investors are not that worried about Sebon advice.</p>

<p><strong>Fewer financial instruments</strong><br />

Except for trading of equities and mutual funds lately, investors in the stock market do not have other financial instruments available for trading.</p>

<p>Lack of freely tradable financial products has not only inhibited the growth of the stock market but also posed a challenge for investors to complete their portfolio. While government-issued bond are listed in the secondary market, they are not freely tradable due to various reasons. In recent days, debentures issued by banks are also being traded in the market. However, the volume of debentures’ trading in the market is also very low.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard19%2823%29.jpg" style="float:right; height:421px; margin:10px; width:250px" />“The market can have depth only if it has a variety of financial instruments available for trading. This also gives investors, who want to take greater risks, some room in the market,” says Krishna Giri, Chief Operating Officer at Prabhu Capital Ltd.</p>

<p>According to Giri, derivatives, exchange traded funds (ETFs), real estate investment traded funds (REITs) and government-issued instruments including provincial and municipal bonds are some of the financial products that can be introduced in the stock market. It will take less than a year to start preparing for this and actually making such scrips available. </p>

<p>He says that Sebon and Nepse should take a lead role in introducing these financial instruments in the market.</p>

<p>“If the regulator and Nepse show willingness, it is possible to have many of these instruments in the market for trading in six months to a year,” he says, pointing out to the need of laying a regulatory groundwork, developing infrastructure and mechanism in the market for their trading. “But the question is whether the regulator and the stock exchange company are ready to do that.”</p>

<p>Sebon’s Executive Director Giri says that the regulatory body is ready to help facilitate in introducing more financial products in the market. “It's not that the regulator would introduce these new instruments. It is the stock exchange company which should take the lead based on the market demands as well as for the sake of its own business. If there is any lack of regulation, or any rule has stood as an obstacle in the entry of such products, we are ready to address those regulatory issues,” he says.</p>

<p>According to Nepse officials, they are planning to introduce derivatives in the stock market in the ‘near future’.</p>

<p>“We carried out research on the possibility of introducing derivative products in the market. The research report’s conclusion is that derivatives with both index and securities features can be allowed in the market. We now have to amend the trading bylaws to pave the way for introducing this facility in the market,” says Murahari Parajuli, spokesperson of Nepse.</p>

<p>However, analysts cast doubt on the preparation of Nepse to introduce new instruments in the market as its plans like trading of rights entitlements (rights to buy right shares) are yet to materialize.</p>

',

'status' => true,

'publish_date' => null,

'created' => '2021-06-30 08:56:25',

'modified' => '2021-07-05 18:31:10',

'keywords' => '',

'description' => '',

'sortorder' => '3001',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1024',

'image' => '20210630053648_COVER11.jpg',

'sortorder' => '1571',

'published' => true,

'created' => '2021-06-30 05:36:48',

'modified' => '2021-07-05 18:34:54',

'title' => 'July 2021',

'publish_date' => '2021-06-30',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '3051',

'magazine_issue_id' => '1024',

'magazine_category_id' => '21',

'title' => 'Riding THE BOOM',

'image' => '20210630085625_Clipboard11.jpg',

'short_content' => 'Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.',

'content' => '<p><strong>--BY SAGAR GHIMIRE</strong></p>

<p>There is not a single sector in the economy in the last one and a half years that has not borne the brunt of the Covid-19 pandemic.</p>

<p>Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.</p>

<p>Businesses and industries either closed down or operated below their capacity as authorities imposed a nationwide lockdown for four months (between March 24 and July 21 in 2020) last year to contain the spread of the virus. The latest prohibitory orders, which were imposed in April, continue to be in place in many parts of the country to combat the deadly second wave of Covid-19.</p>

<p>As almost all sectors including tourism, retail businesses, manufacturing, foreign trade, construction, education and transportation were hit by the pandemic, the economic growth of the country for the first time in many years observed a contraction of two percent in the last fiscal year (2020/21), according to the Central Bureau of Statistics (CBS).</p>

<p>Amid this gloom, one sector of the economy, however, stood out as an exception: the stock market.</p>

<p>Prices of stocks of listed companies in Nepal Stock Exchange (Nepse), the only stock exchange in the country, have been on an upward trend for last one and a half years. In line with the rise in the Nepse benchmark index which has been recording fresh highs in recent days, most of the stocks listed in the market have seen huge gains in their values during this boom.</p>

<p>The Nepse benchmark index climbed up to an all-time-high of 3,025.83 points on June 14. There was also a surge in both daily transactions and turnover in the stock market. Market capitalization—the total value of all listed companies based on their trading price—also reached Rs 4,216 billion on June 14, which means the total value of the stock market is equal to the size of the country’s overall economy as measured through Gross Domestic Product (GDP). Nepal’s projected GDP in the current fiscal year (2020/21) stands at Rs 4,266.3 billion, according to the CBS.</p>

<p>Market analysts point to a number of factors that have fueled the stock market boom including cheaper bank interest rates, lack of alternate investment avenues for investors and entry of new investors in the market in droves. </p>

<p>While the bull run, as it is known in the stock market parlance for a continuous rise of stocks, has increased the value of the assets that investors hold in the form of securities, at least on paper, the market rally has also raised eyebrows.</p>

<p>The disconnect between the stock market and the real economy has left analysts questioning the sustainability of the rally.</p>

<p>Most of the stocks’ upward movement in the secondary market is largely detached from the performance of the companies. Even those loss-making companies with weak financial indicators have seen their share price soaring in the secondary market.</p>

<p>Ankhukhola Hydropower Company Ltd exemplifies this trend in the stock market. According to the company’s third quarterly financial results for the current fiscal year, its net worth per share is Rs 64.05 and earnings per share (EPS) is minus 13.89. The loss-making hydropower company has not even been in a position to distribute dividends to its shareholders for at least a few years. However, investors do not seem to be bothered by the company’s performance. The buying spree in the market sent the share price up to a record high of Rs 335 on June 14. </p>

<p>Though this company is still to start generating electricity and earning revenue, and the investors may be buying this company’s shares in anticipation of future profits, the current share prices of this company are much higher than that can be justified. </p>

<p>Similar is the case with many other stocks. Regardless of their performance, almost all companies listed in the Nepse have witnessed the value of their stocks soaring during the market rally. It is despite the fact that the pandemic has either dealt a heavy blow to most of the listed companies or affected their bottom line.</p>

<p>Still, investors are continuing to pour money into those stocks to propel the stock market to the peak, shrugging off concerns of ‘unjustified bullish sentiment’.</p>

<p>Analysts suggest that the performance of the economy or fundamentals of a company may not always dictate the course of the market.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard13%2829%29.jpg" style="float:right; height:428px; margin:10px; width:250px" />“Like in the current scenario of our market, it’s not the fundamentals or the course of the economy that always drives the rally. Higher valuation of stocks also reflects the bullish sentiment of investors or their future expectations from those companies and the recent policy easing that favours companies and investors. This happens also in stock markets in other countries,” says Prakash Tiwari, a stock market analyst.</p>

<p>From Dow Jones, S&P 500 and Nasdaq Composite index of the US to Nikkei 225 of Tokyo Stock Exchange to FTSE 100 of the London Stock Exchange to BSE Sensex and Nifty in India, most of the stock markets around the world surged during the pandemic.</p>

<p>“There are various factors at play,” says Tiwari. </p>

<p>One major factor is the low interest rate of banking institutions.</p>

<p>Amid a sharp decline in economic activity during the pandemic which has depressed the demand for loans, banks and financial institutions (BFIs) are slashing their interest rates. Interest rates in both saving accounts and fixed deposits have also gone down sharply. Awash with liquidity, BFIs, which were competing with each other to attract deposits until a few years ago due to shortage of lendable funds, are even reluctant to accept deposits at more than three percent on savings accounts and seven percent on one-year fixed deposits.</p>

<p>According to the Nepal Rastra Bank’s statistics, the weighted average interest rate on credit stood at 8.53 percent in mid-May compared to 12.22 percent two years ago. The weighted average interest rate on deposit also fell to 4.81 percent from 6.67 percent.</p>

<p>While the pandemic either discouraged or restricted investments in other businesses or projects for investors, the stock market, already on an upward trend, emerged as a promising avenue. Various measures introduced by the government and the NRB to ease the policies and provide relief to businesses and enterprises battered by the pandemic also supported the stock market rally.</p>

<p>“People were shut in their homes due to the lockdown or prohibitory orders. At the same time, Nepse implemented a system allowing investors to trade stocks online. With reduction in spending due to the lockdown, low interest rates and no other avenues like real estate or businesses for investment, they were hearing or seeing stock prices going up and up,” says Tiwari. “They felt like they would miss the boat if they did not immediately jump into the market. But they should be aware about financial risks in the market. It's not always bullish, but sometimes brutally bearish also.”</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard14%2845%29.jpg" style="height:462px; width:800px" /></p>

<p><strong>Stock market gold rush </strong><br />

After returning from the UK a few years ago, Shambu Dhital, 36, was planning to open a restaurant in Kathmandu from his savings. However, he gave up his business plan after the coronavirus swept across the country.</p>

<p>Disappointed with the low interest rates on fixed deposits, he decided to pour his money into some insurance and hydropower stocks on the advice of one of his friends who was ‘also making money’ in the market, he says. He claims that the value of stocks that he picked with the help of his friends has nearly doubled in the last six months. He, however, declines to divulge the details of his investment.</p>

<p>“The value of my shares has doubled. This level of gain would not have been possible if I had invested it in opening a restaurant,” says Dhital. </p>

<p>Stock brokers say that there has been a huge growth in the number of investors in recent months, particularly during the prohibitory period when Covid-19 containment measures closed the physical floors of brokerage firms for investors and trading went completely online.</p>

<p>Though there is no exact figure of stock investors in the country, online accounts created by brokerage firms give an estimate of those who were actively trading during the pandemic. </p>

<p>According to Nepse, 703,885 online accounts have been created, a majority of them in the last three months when many parts of the country including the Kathmandu Valley were closed due to prohibitory orders.</p>

<p>Adoption of technology for trading facilitated the surge of new investors.</p>

<p>Compared to the lengthy process of visiting the trading floors of brokerage firms to manually fill out forms and place buy or sell orders of shares, it all went online. Many investors, not allowed to step out of their homes due to the prohibitory orders, were now glued to their computers or mobiles to watch the movement of stock prices in the secondary market. From Facebook groups to rooms of new voice-only social media app ClubHouse, discussions were flooded with investors looking for stock market basics, tips and trends about investment.</p>

<p>However, the stock market did not start attracting the public only after the trading went online. With the implementation of the full-fledged dematerialised form of share trading system in 2016 and the facility to apply shares through Mero Share app, public offerings of various companies were already attracting an overwhelming number of investors. As most of the companies were floating their primary shares at a face value of Rs 100, which would eventually rise multifold in the secondary market, they were selling like hotcakes. The adoption of a full-fledged online system in stock trading has given an impetus to the growth of the market. Thanks to the online trading system, the share market, which was largely limited to the Kathmandu Valley, has now expanded to other parts of the country to some extent.</p>

<p>Brokers say that some Nepalis who are working abroad have also been trading in the stock market in recent days. </p>

<p>The recent volume of daily transactions and market turnover also partly reflects a significant growth in the number of investors. The daily transaction amount, number of transactions and number of traded shares have also jumped by multifold in recent months.</p>

<p>According to Nepse, the stock market recorded a daily turnover of Rs 13.94 billion from the trading of 29.52 million units of shares through 139,247 transactions per day on an average in the month of Jesth (between mid-May and mid-June) this year. In the same month two years ago, Rs 822 million worth of 2.61 million units of shares changed hands through 9,939 transactions on an average daily. On June 13, the stock market recorded the all-time-high daily turnover of Rs 19.55 billion.</p>

<p>“While the growth in the turnover is largely attributed to the surge in stock prices, the rise in the number of transactions and traded shares also show that there is a significant growth in the number of investors in the market,” says Priya Raj Regmi, former president of Stock Brokers Association of Nepal (SBAN). </p>

<p>Retail penetration not only helps expand the investors’ base but also provides more depth to the market. Nonetheless, the way these new investors are jumping into the market also has its downsides.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard16%2831%29.jpg" style="float:right; height:410px; margin:10px; width:250px" />“While the surge of new investors helps in strengthening the base of the stock market in the long-term, they are also prone to making poor investment decisions based on speculations and rumours as we can often see in their irrational behaviour in the market. A faster ride also comes with higher risk,” says Mekh Bahadur Thapa, chairman of Merchant Bankers Association of Nepal (MBAN).</p>

<p>Pointing out to a risk of an exodus of investors when there is even a slight correction in the market, he underscores the need for massive awareness and education programmes which he says will help investors make informed investment decisions and prepare them for the adverse market scenario.</p>

<p>But the growing clout of mutual funds and other bigger players in the stock market is expected to reduce the volatility in the market to some extent. This was not the case a few years ago due to their limited number and investment capacity. There are now 22 mutual fund schemes with a portfolio of over Rs 22 billion. There are also insurance companies active on share trading. Some business houses also have reportedly entered the market during the recent boom. As they make investment decisions largely based on fundamental and technical analysis, they could play a significant role in reducing market volatility, according to experts.</p>

<p>“Every market has its cycle. Nobody can completely rule out a worse scenario in the market. However, mutual funds’ number and size have gone up in recent years. They make investments based on fundamental analysis which can help stabilise the market to a certain extent during the volatility,” says Thapa. </p>

<p>Concerns over the longevity of the boom are being raised as the stock market has never witnessed such a huge growth at such a short interval of time. The previous bull run that had started in 2012had continued till 2016 with Nepse index jumping nearly six times. But this time it had increased 2.7 times within 19 months.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard15%2834%29.jpg" style="height:390px; width:800px" /></p>

<p><strong>Ending dominance of banking sector</strong><br />

The stock market is largely dominated by banks and financial institutions. Nearly two-thirds of listed companies are banks and financial institutions (BFIs). The dominance of the banking sector has often prompted the market to move based on the decision or policy of the NRB. Investors also complain that they are facing problems diversifying their portfolio due to the low presence of non-banking scrips. The entry of real sector companies in the market is also expected to counterbalance the dominance of the banking sector. </p>

<p>Those who do not want higher exposure to banking scrips are currently left with little choice when investing in the market. Realising that the stock market has failed to represent all sectors of the economy, the government has taken some measures including the offer to provide income tax rebates to rope in companies from various sectors. </p>

<p>The government even tried to make listings mandatory for certain companies similar to banks and insurance companies.</p>

<p>The government also seems to have abandoned the plan to make it mandatory for manufacturing companies that have capital of more than Rs 1 billion to get listed in the stock market. The plan was announced in the budget speech of fiscal year 2018/19, but the government has not taken any further initiatives for this since then except that the Ministry of Finance had asked the Company Registrar’s Office to provide the list of companies that have capital more than Rs. 1 billion.</p>

<p>The majority of the newly listed companies are still from the banking or insurance sectors. In recent years, hydropower companies have also been at the forefront of public offerings. However, companies from the manufacturing, hospitality, education and other sectors have not shown much interest in the listing.</p>

<p>Except for Shivam Cement Ltd and Chandragiri Hills Ltd, all two dozen companies which were listed in Nepse in the last two years are either from the banking and insurance or hydropower sectors.</p>

<p>One of the major factors discouraging companies from making a public offering has been the share pricing system which was making it either impossible or extremely difficult for companies to sell their shares at a price higher than the face value of Rs 100.</p>

<p>While Securities Board of Nepal (Sebon) has started to allow issuing IPOs at a premium since 2016 after the enactment of Securities Registration and Issue Regulation, many companies were finding it difficult to qualify for that privilege. However, Sebon decision to introduce the book building method is expected to facilitate it though it is yet to be tested.</p>

<p>When it comes to the pricing system, Sebon was always under pressure from two extremes: the mass that always stood against ending the long-standing practice of pricing primary shares at a face value of 100 and the promoters looking for a free hand in determining the premium of their companies’ shares, according to market experts. </p>

<p>“As Sebon was caught between these two extremes, we could not have a stable policy on the pricing of shares. There was a public offering at face value. Then, we also have a policy on allowing offering shares at a premium with strict provisions,” says Mekh Bahadur Thapa, Chairman of Merchant Bankers Association of Nepal (MBAN). </p>

<p>Those companies who are financially doing well were always concerned with the pricing system of floating shares at Rs 100, according to Thapa. “Now, Sebon has introduced the book building method which is an internationally accepted practice of determining share prices based on a bidding process. This will encourage better companies to list themselves and increase the share of the non-banking sector in the stock market,” says Thapa, who is also Deputy CEO of NIBL Ace Capital.</p>

<p>Two manufacturing companies—Reliance Spinning Mills and Sarbottam Cement—are now in the process of floating their shares based on the newly introduced book building method.</p>

<p>Investors and the public also expect the initial public offering (IPO) of the first private mobile service provider Ncell in the near future. While Ncell has not officially confirmed or denied its IPO plan, the mobile service provider’s recent decision to convert into a public limited company has been interpreted as its intention to list itself on the stock market. The listing of the largest private sector mobile service provider will also help in reducing the dominance of the banking sector in the stock market.</p>

<p>“Diversity of listed companies in the market helps investors in managing market volatility. The government and Sebon should create a favourable environment for companies from various sectors for their stock listing,” says Thapa.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard20%2818%29.jpg" style="height:440px; width:800px" /></p>

<p><strong>Regulator’s roles for reforms</strong><br />

While a number of reform measures have been implemented in recent years, experts say that the government and Sebon are too slow to act on the basis of the market’s needs. It took years for the government to phase out paperless trading in the securities market that was still in place until 2014.</p>

<p>After implementing a full-fledged dematerialised system from 2016, Nepse introduced the internet-based NEPSE Online Trading System (NOTS) in 2018, paving the way for investors to carry out trading online. Eliminating the cumbersome manual process in the IPO, ‘Mero Share’ was introduced that not only allowed investors to participate in the public offering through the internet but also attracted the public to the capital market.</p>

<p>Though the stock market is still considered a laggard in terms of technological revolution, the gradual adoption of technology is making trading of securities convenient, lowering costs and expanding the reach of investors, according to experts. However, frequent technical glitches on day-to-day trading, cybersecurity vulnerabilities and lack of capacity of many investors, brokers and regulators to embrace the new system have posed a challenge and stopped the sector from taking full advantage of the technological advancements in the market. The privatisation of Nepse, which is owned by the government, is long overdue. Promises to open the stock market for non-resident Nepalis are yet to materialise.</p>

<p>According to analysts, Sebon is struggling to keep up with the market growth. Due to its weak capacity of surveillance and enforcement, it has failed to crackdown on various market anomalies including cases of insider trading, cornering and stock manipulation.</p>

<p>Sebon often faces criticisms for failing to play the regulatory role effectively as it did recently.</p>

<p>A recent decision of Sebon to list 51 companies as ‘risky’ stocks (including Ankhu Khola, the case cited above) sparked anger among investors and analysts. In its statement issued amid a stock market boom, Sebon on June 15 not only announced that it was investigating insider trading, circular trading and cornering in those 51 scrips, but also urged investors to consider its list while making investment decisions.</p>

<p>Not for the first time has Sebon weighed in with its appeal to investors to tread cautiously in the market.</p>

<p>While earlier statements used to be limited to urging investors to invest on the basis of informed decisions, Sebon this time went a step further to single out 51 scrips as ‘risky’, citing its preliminary analysis.</p>

<p>Such a ‘knee jerk reaction’ to the stock movement is unbecoming of the regulator, say analysts.</p>

<p>“The government or a regulator should become a referee to ensure that there is fair play in the market. It must not become a player itself. There are so many things that it has to prioritise including continued surveillance, investment in software and issuing brokerage licenses to new companies,” says Biswo Poudel, an economist. “Rather than reacting to the stock price movement, the regulator should focus on market reforms,” he says. </p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard18%2830%29.jpg" style="float:right; height:431px; margin:10px; width:250px" />Sebon officials, however, defend the move. “Of course, there are many things that Sebon has to do for the development of the securities market in the country. What we should not forget is that we also have a responsibility of protecting investors’ interest. So, it’s our duty to urge them to remain cautious,” says Niraj Giri, Sebon’s Executive Director and Spokesperson. “The list that we have published is based on our analysis of certain parameters and indicators. We have a duty to ask investors to become cautious while making investment decisions. We have asked them to just separate the wheat from the chaff,” says Giri.</p>

<p>But, nowhere in the world does a stock market regulator publish a list of companies saying it’s over valued based on PE ratio or net worth, say stock market analysts. For example, Amazon and other companies listed in the US stock markets have been trading at price way higher than its price to earningratio, but the US Securities and Exchange Commission (SEC) has never come up with such a list.</p>

<p>For them, the Sebon’s statement is akin to NRB publishing a list of banks terming them ‘risky’ and asking depositors to be cautious while choosing banks to park their money.</p>

<p>However, Sebon’s move did cause the market to reverse, though it seems only a temporary decline. After the release of the statement, Nepse benchmark index took a dive of over 120 points, or3.97 percent, in mere three trading days. Analysts say that the decline reflects the reaction of investors who were worried with the regulator’s perception towards the stock market rally. However, the market started showing revival on June 22, indicating that the investors are not that worried about Sebon advice.</p>

<p><strong>Fewer financial instruments</strong><br />

Except for trading of equities and mutual funds lately, investors in the stock market do not have other financial instruments available for trading.</p>

<p>Lack of freely tradable financial products has not only inhibited the growth of the stock market but also posed a challenge for investors to complete their portfolio. While government-issued bond are listed in the secondary market, they are not freely tradable due to various reasons. In recent days, debentures issued by banks are also being traded in the market. However, the volume of debentures’ trading in the market is also very low.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard19%2823%29.jpg" style="float:right; height:421px; margin:10px; width:250px" />“The market can have depth only if it has a variety of financial instruments available for trading. This also gives investors, who want to take greater risks, some room in the market,” says Krishna Giri, Chief Operating Officer at Prabhu Capital Ltd.</p>

<p>According to Giri, derivatives, exchange traded funds (ETFs), real estate investment traded funds (REITs) and government-issued instruments including provincial and municipal bonds are some of the financial products that can be introduced in the stock market. It will take less than a year to start preparing for this and actually making such scrips available. </p>

<p>He says that Sebon and Nepse should take a lead role in introducing these financial instruments in the market.</p>

<p>“If the regulator and Nepse show willingness, it is possible to have many of these instruments in the market for trading in six months to a year,” he says, pointing out to the need of laying a regulatory groundwork, developing infrastructure and mechanism in the market for their trading. “But the question is whether the regulator and the stock exchange company are ready to do that.”</p>

<p>Sebon’s Executive Director Giri says that the regulatory body is ready to help facilitate in introducing more financial products in the market. “It's not that the regulator would introduce these new instruments. It is the stock exchange company which should take the lead based on the market demands as well as for the sake of its own business. If there is any lack of regulation, or any rule has stood as an obstacle in the entry of such products, we are ready to address those regulatory issues,” he says.</p>

<p>According to Nepse officials, they are planning to introduce derivatives in the stock market in the ‘near future’.</p>

<p>“We carried out research on the possibility of introducing derivative products in the market. The research report’s conclusion is that derivatives with both index and securities features can be allowed in the market. We now have to amend the trading bylaws to pave the way for introducing this facility in the market,” says Murahari Parajuli, spokesperson of Nepse.</p>

<p>However, analysts cast doubt on the preparation of Nepse to introduce new instruments in the market as its plans like trading of rights entitlements (rights to buy right shares) are yet to materialize.</p>

',

'status' => true,

'publish_date' => null,

'created' => '2021-06-30 08:56:25',

'modified' => '2021-07-05 18:31:10',

'keywords' => '',

'description' => '',

'sortorder' => '3001',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1024',

'image' => '20210630053648_COVER11.jpg',

'sortorder' => '1571',

'published' => true,

'created' => '2021-06-30 05:36:48',

'modified' => '2021-07-05 18:34:54',

'title' => 'July 2021',

'publish_date' => '2021-06-30',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '3051',

'hit' => '2631'

)

)

)

$current_user = null

$logged_in = false

$user = null

include - APP/View/MagazineArticles/view.ctp, line 54

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Trying to access array offset on value of type null [APP/View/MagazineArticles/view.ctp, line 54]

$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '3051',

'magazine_issue_id' => '1024',

'magazine_category_id' => '21',

'title' => 'Riding THE BOOM',

'image' => '20210630085625_Clipboard11.jpg',

'short_content' => 'Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.',

'content' => '<p><strong>--BY SAGAR GHIMIRE</strong></p>

<p>There is not a single sector in the economy in the last one and a half years that has not borne the brunt of the Covid-19 pandemic.</p>

<p>Coronavirus raging across the country not only sickened hundreds of thousands of people and claimed over 8,558 lives across the country but also brought economic activity almost to a standstill for months.</p>

<p>Businesses and industries either closed down or operated below their capacity as authorities imposed a nationwide lockdown for four months (between March 24 and July 21 in 2020) last year to contain the spread of the virus. The latest prohibitory orders, which were imposed in April, continue to be in place in many parts of the country to combat the deadly second wave of Covid-19.</p>

<p>As almost all sectors including tourism, retail businesses, manufacturing, foreign trade, construction, education and transportation were hit by the pandemic, the economic growth of the country for the first time in many years observed a contraction of two percent in the last fiscal year (2020/21), according to the Central Bureau of Statistics (CBS).</p>

<p>Amid this gloom, one sector of the economy, however, stood out as an exception: the stock market.</p>

<p>Prices of stocks of listed companies in Nepal Stock Exchange (Nepse), the only stock exchange in the country, have been on an upward trend for last one and a half years. In line with the rise in the Nepse benchmark index which has been recording fresh highs in recent days, most of the stocks listed in the market have seen huge gains in their values during this boom.</p>

<p>The Nepse benchmark index climbed up to an all-time-high of 3,025.83 points on June 14. There was also a surge in both daily transactions and turnover in the stock market. Market capitalization—the total value of all listed companies based on their trading price—also reached Rs 4,216 billion on June 14, which means the total value of the stock market is equal to the size of the country’s overall economy as measured through Gross Domestic Product (GDP). Nepal’s projected GDP in the current fiscal year (2020/21) stands at Rs 4,266.3 billion, according to the CBS.</p>

<p>Market analysts point to a number of factors that have fueled the stock market boom including cheaper bank interest rates, lack of alternate investment avenues for investors and entry of new investors in the market in droves. </p>

<p>While the bull run, as it is known in the stock market parlance for a continuous rise of stocks, has increased the value of the assets that investors hold in the form of securities, at least on paper, the market rally has also raised eyebrows.</p>

<p>The disconnect between the stock market and the real economy has left analysts questioning the sustainability of the rally.</p>

<p>Most of the stocks’ upward movement in the secondary market is largely detached from the performance of the companies. Even those loss-making companies with weak financial indicators have seen their share price soaring in the secondary market.</p>

<p>Ankhukhola Hydropower Company Ltd exemplifies this trend in the stock market. According to the company’s third quarterly financial results for the current fiscal year, its net worth per share is Rs 64.05 and earnings per share (EPS) is minus 13.89. The loss-making hydropower company has not even been in a position to distribute dividends to its shareholders for at least a few years. However, investors do not seem to be bothered by the company’s performance. The buying spree in the market sent the share price up to a record high of Rs 335 on June 14. </p>

<p>Though this company is still to start generating electricity and earning revenue, and the investors may be buying this company’s shares in anticipation of future profits, the current share prices of this company are much higher than that can be justified. </p>

<p>Similar is the case with many other stocks. Regardless of their performance, almost all companies listed in the Nepse have witnessed the value of their stocks soaring during the market rally. It is despite the fact that the pandemic has either dealt a heavy blow to most of the listed companies or affected their bottom line.</p>

<p>Still, investors are continuing to pour money into those stocks to propel the stock market to the peak, shrugging off concerns of ‘unjustified bullish sentiment’.</p>

<p>Analysts suggest that the performance of the economy or fundamentals of a company may not always dictate the course of the market.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard13%2829%29.jpg" style="float:right; height:428px; margin:10px; width:250px" />“Like in the current scenario of our market, it’s not the fundamentals or the course of the economy that always drives the rally. Higher valuation of stocks also reflects the bullish sentiment of investors or their future expectations from those companies and the recent policy easing that favours companies and investors. This happens also in stock markets in other countries,” says Prakash Tiwari, a stock market analyst.</p>

<p>From Dow Jones, S&P 500 and Nasdaq Composite index of the US to Nikkei 225 of Tokyo Stock Exchange to FTSE 100 of the London Stock Exchange to BSE Sensex and Nifty in India, most of the stock markets around the world surged during the pandemic.</p>

<p>“There are various factors at play,” says Tiwari. </p>

<p>One major factor is the low interest rate of banking institutions.</p>

<p>Amid a sharp decline in economic activity during the pandemic which has depressed the demand for loans, banks and financial institutions (BFIs) are slashing their interest rates. Interest rates in both saving accounts and fixed deposits have also gone down sharply. Awash with liquidity, BFIs, which were competing with each other to attract deposits until a few years ago due to shortage of lendable funds, are even reluctant to accept deposits at more than three percent on savings accounts and seven percent on one-year fixed deposits.</p>

<p>According to the Nepal Rastra Bank’s statistics, the weighted average interest rate on credit stood at 8.53 percent in mid-May compared to 12.22 percent two years ago. The weighted average interest rate on deposit also fell to 4.81 percent from 6.67 percent.</p>

<p>While the pandemic either discouraged or restricted investments in other businesses or projects for investors, the stock market, already on an upward trend, emerged as a promising avenue. Various measures introduced by the government and the NRB to ease the policies and provide relief to businesses and enterprises battered by the pandemic also supported the stock market rally.</p>

<p>“People were shut in their homes due to the lockdown or prohibitory orders. At the same time, Nepse implemented a system allowing investors to trade stocks online. With reduction in spending due to the lockdown, low interest rates and no other avenues like real estate or businesses for investment, they were hearing or seeing stock prices going up and up,” says Tiwari. “They felt like they would miss the boat if they did not immediately jump into the market. But they should be aware about financial risks in the market. It's not always bullish, but sometimes brutally bearish also.”</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard14%2845%29.jpg" style="height:462px; width:800px" /></p>

<p><strong>Stock market gold rush </strong><br />

After returning from the UK a few years ago, Shambu Dhital, 36, was planning to open a restaurant in Kathmandu from his savings. However, he gave up his business plan after the coronavirus swept across the country.</p>

<p>Disappointed with the low interest rates on fixed deposits, he decided to pour his money into some insurance and hydropower stocks on the advice of one of his friends who was ‘also making money’ in the market, he says. He claims that the value of stocks that he picked with the help of his friends has nearly doubled in the last six months. He, however, declines to divulge the details of his investment.</p>

<p>“The value of my shares has doubled. This level of gain would not have been possible if I had invested it in opening a restaurant,” says Dhital. </p>

<p>Stock brokers say that there has been a huge growth in the number of investors in recent months, particularly during the prohibitory period when Covid-19 containment measures closed the physical floors of brokerage firms for investors and trading went completely online.</p>

<p>Though there is no exact figure of stock investors in the country, online accounts created by brokerage firms give an estimate of those who were actively trading during the pandemic. </p>

<p>According to Nepse, 703,885 online accounts have been created, a majority of them in the last three months when many parts of the country including the Kathmandu Valley were closed due to prohibitory orders.</p>

<p>Adoption of technology for trading facilitated the surge of new investors.</p>

<p>Compared to the lengthy process of visiting the trading floors of brokerage firms to manually fill out forms and place buy or sell orders of shares, it all went online. Many investors, not allowed to step out of their homes due to the prohibitory orders, were now glued to their computers or mobiles to watch the movement of stock prices in the secondary market. From Facebook groups to rooms of new voice-only social media app ClubHouse, discussions were flooded with investors looking for stock market basics, tips and trends about investment.</p>

<p>However, the stock market did not start attracting the public only after the trading went online. With the implementation of the full-fledged dematerialised form of share trading system in 2016 and the facility to apply shares through Mero Share app, public offerings of various companies were already attracting an overwhelming number of investors. As most of the companies were floating their primary shares at a face value of Rs 100, which would eventually rise multifold in the secondary market, they were selling like hotcakes. The adoption of a full-fledged online system in stock trading has given an impetus to the growth of the market. Thanks to the online trading system, the share market, which was largely limited to the Kathmandu Valley, has now expanded to other parts of the country to some extent.</p>

<p>Brokers say that some Nepalis who are working abroad have also been trading in the stock market in recent days. </p>

<p>The recent volume of daily transactions and market turnover also partly reflects a significant growth in the number of investors. The daily transaction amount, number of transactions and number of traded shares have also jumped by multifold in recent months.</p>

<p>According to Nepse, the stock market recorded a daily turnover of Rs 13.94 billion from the trading of 29.52 million units of shares through 139,247 transactions per day on an average in the month of Jesth (between mid-May and mid-June) this year. In the same month two years ago, Rs 822 million worth of 2.61 million units of shares changed hands through 9,939 transactions on an average daily. On June 13, the stock market recorded the all-time-high daily turnover of Rs 19.55 billion.</p>

<p>“While the growth in the turnover is largely attributed to the surge in stock prices, the rise in the number of transactions and traded shares also show that there is a significant growth in the number of investors in the market,” says Priya Raj Regmi, former president of Stock Brokers Association of Nepal (SBAN). </p>

<p>Retail penetration not only helps expand the investors’ base but also provides more depth to the market. Nonetheless, the way these new investors are jumping into the market also has its downsides.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard16%2831%29.jpg" style="float:right; height:410px; margin:10px; width:250px" />“While the surge of new investors helps in strengthening the base of the stock market in the long-term, they are also prone to making poor investment decisions based on speculations and rumours as we can often see in their irrational behaviour in the market. A faster ride also comes with higher risk,” says Mekh Bahadur Thapa, chairman of Merchant Bankers Association of Nepal (MBAN).</p>

<p>Pointing out to a risk of an exodus of investors when there is even a slight correction in the market, he underscores the need for massive awareness and education programmes which he says will help investors make informed investment decisions and prepare them for the adverse market scenario.</p>

<p>But the growing clout of mutual funds and other bigger players in the stock market is expected to reduce the volatility in the market to some extent. This was not the case a few years ago due to their limited number and investment capacity. There are now 22 mutual fund schemes with a portfolio of over Rs 22 billion. There are also insurance companies active on share trading. Some business houses also have reportedly entered the market during the recent boom. As they make investment decisions largely based on fundamental and technical analysis, they could play a significant role in reducing market volatility, according to experts.</p>

<p>“Every market has its cycle. Nobody can completely rule out a worse scenario in the market. However, mutual funds’ number and size have gone up in recent years. They make investments based on fundamental analysis which can help stabilise the market to a certain extent during the volatility,” says Thapa. </p>

<p>Concerns over the longevity of the boom are being raised as the stock market has never witnessed such a huge growth at such a short interval of time. The previous bull run that had started in 2012had continued till 2016 with Nepse index jumping nearly six times. But this time it had increased 2.7 times within 19 months.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard15%2834%29.jpg" style="height:390px; width:800px" /></p>

<p><strong>Ending dominance of banking sector</strong><br />

The stock market is largely dominated by banks and financial institutions. Nearly two-thirds of listed companies are banks and financial institutions (BFIs). The dominance of the banking sector has often prompted the market to move based on the decision or policy of the NRB. Investors also complain that they are facing problems diversifying their portfolio due to the low presence of non-banking scrips. The entry of real sector companies in the market is also expected to counterbalance the dominance of the banking sector. </p>

<p>Those who do not want higher exposure to banking scrips are currently left with little choice when investing in the market. Realising that the stock market has failed to represent all sectors of the economy, the government has taken some measures including the offer to provide income tax rebates to rope in companies from various sectors. </p>

<p>The government even tried to make listings mandatory for certain companies similar to banks and insurance companies.</p>

<p>The government also seems to have abandoned the plan to make it mandatory for manufacturing companies that have capital of more than Rs 1 billion to get listed in the stock market. The plan was announced in the budget speech of fiscal year 2018/19, but the government has not taken any further initiatives for this since then except that the Ministry of Finance had asked the Company Registrar’s Office to provide the list of companies that have capital more than Rs. 1 billion.</p>

<p>The majority of the newly listed companies are still from the banking or insurance sectors. In recent years, hydropower companies have also been at the forefront of public offerings. However, companies from the manufacturing, hospitality, education and other sectors have not shown much interest in the listing.</p>

<p>Except for Shivam Cement Ltd and Chandragiri Hills Ltd, all two dozen companies which were listed in Nepse in the last two years are either from the banking and insurance or hydropower sectors.</p>

<p>One of the major factors discouraging companies from making a public offering has been the share pricing system which was making it either impossible or extremely difficult for companies to sell their shares at a price higher than the face value of Rs 100.</p>

<p>While Securities Board of Nepal (Sebon) has started to allow issuing IPOs at a premium since 2016 after the enactment of Securities Registration and Issue Regulation, many companies were finding it difficult to qualify for that privilege. However, Sebon decision to introduce the book building method is expected to facilitate it though it is yet to be tested.</p>

<p>When it comes to the pricing system, Sebon was always under pressure from two extremes: the mass that always stood against ending the long-standing practice of pricing primary shares at a face value of 100 and the promoters looking for a free hand in determining the premium of their companies’ shares, according to market experts. </p>

<p>“As Sebon was caught between these two extremes, we could not have a stable policy on the pricing of shares. There was a public offering at face value. Then, we also have a policy on allowing offering shares at a premium with strict provisions,” says Mekh Bahadur Thapa, Chairman of Merchant Bankers Association of Nepal (MBAN). </p>

<p>Those companies who are financially doing well were always concerned with the pricing system of floating shares at Rs 100, according to Thapa. “Now, Sebon has introduced the book building method which is an internationally accepted practice of determining share prices based on a bidding process. This will encourage better companies to list themselves and increase the share of the non-banking sector in the stock market,” says Thapa, who is also Deputy CEO of NIBL Ace Capital.</p>

<p>Two manufacturing companies—Reliance Spinning Mills and Sarbottam Cement—are now in the process of floating their shares based on the newly introduced book building method.</p>