$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

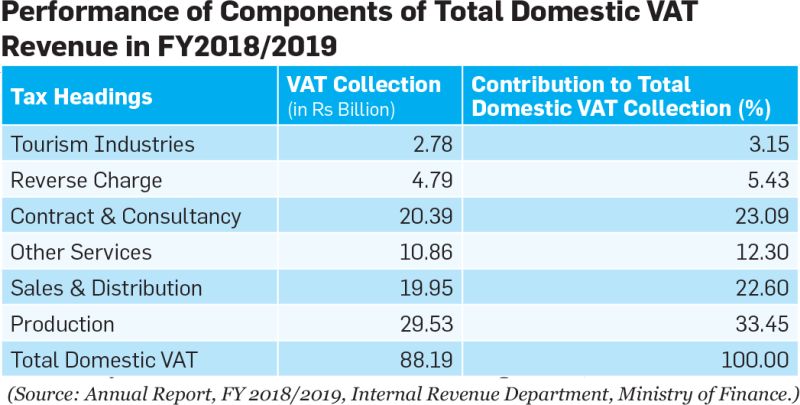

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2749',

'hit' => '3903'

)

)

)

$current_user = null

$logged_in = false

$user = null

include - APP/View/MagazineArticles/view.ctp, line 54

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Trying to access array offset on value of type null [APP/View/MagazineArticles/view.ctp, line 54]

$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2749',

'hit' => '3903'

)

)

)

$current_user = null

$logged_in = false

$user = null

include - APP/View/MagazineArticles/view.ctp, line 54

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Trying to access array offset on value of type null [APP/View/MagazineArticles/view.ctp, line 55]

//find the group of logged user

$groupId = $user['Group']['id'];

$user_id=$user["id"];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2749',

'hit' => '3903'

)

)

)

$current_user = null

$logged_in = false

$user = null

$groupId = null

include - APP/View/MagazineArticles/view.ctp, line 55

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Undefined index: summary [APP/View/MagazineArticles/view.ctp, line 62]

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2749',

'hit' => '3903'

)

)

)

$current_user = null

$logged_in = false

$user = null

$groupId = null

$user_id = null

include - APP/View/MagazineArticles/view.ctp, line 62

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Undefined index: summary [APP/View/MagazineArticles/view.ctp, line 68]

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>

<p>Additionally, tax collectors and tax administrators are powerful in countries like Nepal. This encourages them to exercise their bargaining power to resist reform and to get away with extracting revenues from incompetent or even illegal tax practices for private gain. Therefore, any effective implementation of VAT in Nepal is hampered by the attitude and behaviour of businessmen and the tax administration. The lack of a sense of accountability and responsibility on the part of tax officials has further intensified the problem. These issues of VAT need to be addressed properly and urgently to mobilise the potential VAT revenue in Nepal.</p>

<p>The government needs to take necessary actions and steps to solve the existing problems in the implementation of VAT. It should focus on simplifying tax systems, strengthening the tax administration, and broadening the tax base.</p>

<p>These efforts should be made within a broader reform programme that aims to strengthen governance, improve the business environment and formalise as well as modernise the economy. The government needs full cooperation from the tax administration, the taxpayers and businessmen in its efforts to generate more revenue.</p>

<p>The success of VAT largely depends upon the honesty and morality of tax officials and the business community.</p>

<p><strong><em>The author is a member of the Faculty of Economics at Apex College. He can be reached at kpprasai@gmail.com</em></strong></p>

',

'status' => true,

'publish_date' => null,

'created' => '2020-10-10 14:51:10',

'modified' => '2020-10-10 14:51:10',

'keywords' => '',

'description' => '',

'sortorder' => '2699',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '1006',

'image' => '20201009012318_cover.jpg',

'sortorder' => '1554',

'published' => true,

'created' => '2020-02-24 17:36:43',

'modified' => '2020-10-09 13:24:05',

'title' => 'January 2020',

'publish_date' => '2020-02-24',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '26',

'title' => 'Economy and Policy',

'sortorder' => '534',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2013-03-01 00:00:00'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2749',

'magazine_issue_id' => '1006',

'magazine_category_id' => '26',

'title' => 'Performance of VAT in Nepal',

'image' => '20201010025110_Clipboard29.jpg',

'short_content' => 'Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. ',

'content' => '<p><strong>--BY KP PRASAI</strong></p>

<p>Value Added Tax (VAT), one of the major components of indirect tax, was introduced in Nepal as part of the national tax reform on November 16, 1997 with an objective to increase revenue mobilisation by broadening the tax base and establishing neutrality, efficiency, fairness and transparency in the Nepali tax system. VAT, the largest source of government revenue for some years, was levied in place of the then four different taxes namely, sales tax, hotel tax, contract tax and entertainment tax.</p>

<p>The rate of VAT was fixed at 10 percent when it was first introduced and the amended VAT Act 2005 raised the rate to 13 percent with effect from fiscal year 2005/2006. Currently, VAT is levied at a single rate of 13 percent with various exemptions and a zero rate for exports. The number of VAT registrants was 2,045 at the time of its introduction in 1997, which increased consistently reaching 240,460 in FY2018/2019. The mobilisation of VAT revenue has been on a steady rise since its inception with its collection standing at Rs 241.9 billion in FY2018/2019, which is 6.9 percent of the GDP, 28 percent of the total revenue and 32 percent of the total tax revenue. However, as these gains are based on revenue from remittance-fueled imports, they may not be sustainable.</p>

<p>The total VAT revenue is divided into domestic and import VAT. The collection of domestic and import VAT stood at Rs 88.19 billion and Rs 153.71 billion respectively in FY2018/2019. The share of domestic and import VAT to total VAT revenue remained at 36 percent and 64 percent correspondingly during the last fiscal year.</p>

<p>The performance of VAT is considered good if the share of domestic VAT is greater than that of import VAT revenue. But, the incidence of Nepal’s VAT on international trade which has now peaked to about two-thirds of total VAT collections, is virtually VAT on imports.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard30%2813%29.jpg" style="height:182px; width:800px" /></p>

<p>Compared to India and China and low-income countries, Nepal’s revenue structure is disproportionately moving towards import-based revenues. The International Monetary Fund (IMF) has found high reliance on import-related revenues as one of the severe issues affecting the Nepali tax system. Furthermore, an IMF staff report came up with the finding that the revenue has been growing in recent years on the back of rising consumption and imports which indicates the need for reforms in domestic VAT collection.</p>

<p>Although VAT has been in application for more than two decades in Nepal, the system is not effective today and the revenue mobilisation through VAT is below the potential. Most of the issues and problems concerning the implementation of VAT have been identified which include weak tax administration, lack of professionalism and honesty in businessmen, lack of taxpayers awareness programmes, rampant corruption, lack of culture of issuing and receiving bills at the point of sale and purchase, large number of exemptions and deductions, narrow coverage, poor tax compliance and weak enforcement, large size of the informal economy, cross-border illegal transactions, large size of the rural population, large untaxed agriculture sector, underdeveloped industrial sector, low financial sector development, under-reporting and non-reporting of taxable transactions to the tax office, family-run businesses, low corporate ethics, low taxpayer morale, under-reporting of sales, wide-spread tax evasion, false export claims, submission of false invoices, unreliable accounting, non-registration of firms above the threshold, among others. These factors have kept a large size of th population and economic transactions outside the tax net.</p>

<p><img alt="" src="/app/webroot/userfiles/images/Clipboard31%2815%29.jpg" style="height:405px; width:800px" /></p>