$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2449',

'magazine_issue_id' => '996',

'magazine_category_id' => '21',

'title' => 'Mutual Funds in Nepal : Way Ahead',

'image' => '20190317123055_Clipboard04.jpg',

'short_content' => 'The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. ',

'content' => '<div style="text-align: center;">

<span style="font-size:16px;"><em>Proper policies and strategies are required to develop the mutual fund market and cash in on the opportunities available in Nepal.</em></span></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<strong>--BY TEAM NEWBIZ</strong></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual Fund companies and the schemes they operate are running aground in Nepal. A new way forward has to be charted out for them. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

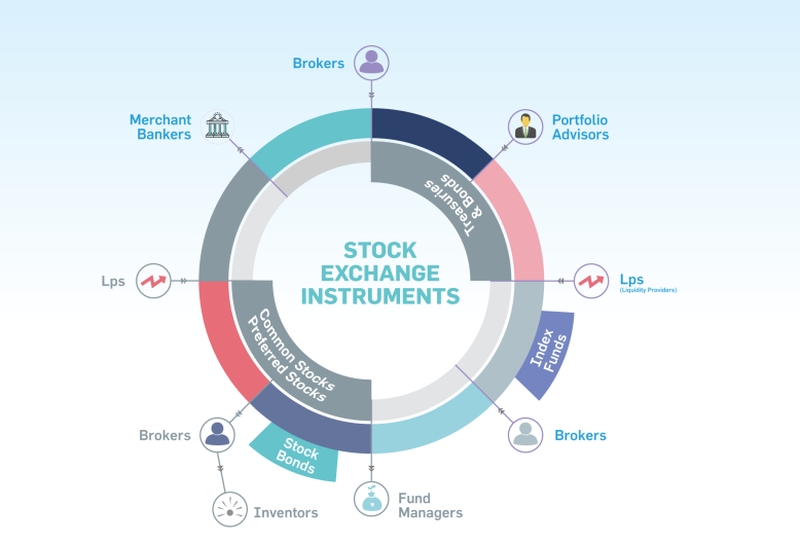

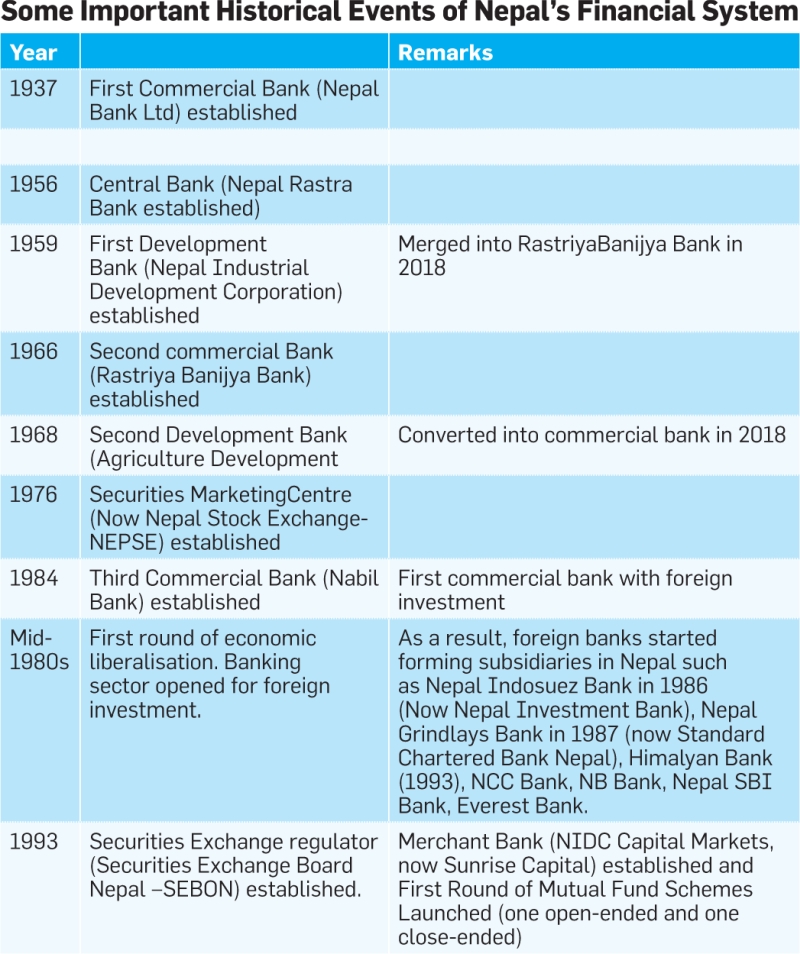

In reality, this is a pathetic state of affairs. Nepal has been historically slow in going ahead with the development of the capital market ecosystem (see box for some historical reference). The stock exchange was started in 1976. It took nearly two decades to start mutual funds and merchant banking companies that operate such funds. Though the number of merchant banks and thus the number of mutual funds in the market has now increased to 13, all the existing mutual fund schemes are close-ended. Though the market started in 1993 with both close-ended and open-ended mutual fund schemes, the new schemes of the open-ended category could not be launched. This has limited the options for the investors and stunted the growth potential of the merchant banks and thereby of the broader capital market. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard07%2813%29.jpg" style="width: 800px; height: 544px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Restrictive Regulation</strong></span></div>

<div style="text-align: justify;">

These fund managers (i.e. merchant banks) are required by the regulator to invest 90 % of the corpus on securities (stock) market – either in the Initial Public Offering (IPO) or from the secondary market. The rest has to be parked as deposits in commercial banks. Thus their Net Asset Value (NAV) totally depends on the performance of the securities market. If the securities market goes up or down, so does the NAV of the mutual funds. Therefore, while the stock market was going up, the mutual funds were doing well and gaining in their NAV and those who invested in these fund units were getting good dividends or capital gain. But in recent months, the market is going down and the NAV of the fund units that were issued at the face value of Rs. 10 has come down to around Rs. 8. This has started scaring the investors away from mutual funds. And the mutual funds are following two strategies. One, they are parking more funds than allowed in bank fixed deposits and paying penalties to the regulator. Second, they are buying more shares from the stock market at reduced prices and improving their average in the hopes that the market will bounce back sometime in the future. However, that is looking much like “Waiting for Godot”. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual funds create small-cap portfolios where small savers, those planning to enter the capital market as investors (both of them have low risk appetite), can invest and learn the ropes of the capital market. When this group of investors get scared away, the growth potential of the capital market gets constrained. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Lack of diversity in the securities listed in the Nepali stock market is one reason for this problem. Almost all the listed securities are shares (equity). Debt instruments (i.e. debentures) are very few and their trade is very rare, thus lacking liquidity. This lack of liquidity demotivates mutual funds from investing in debt instruments. This is one serious problem for the mutual funds when it comes to diversifying their portfolio. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

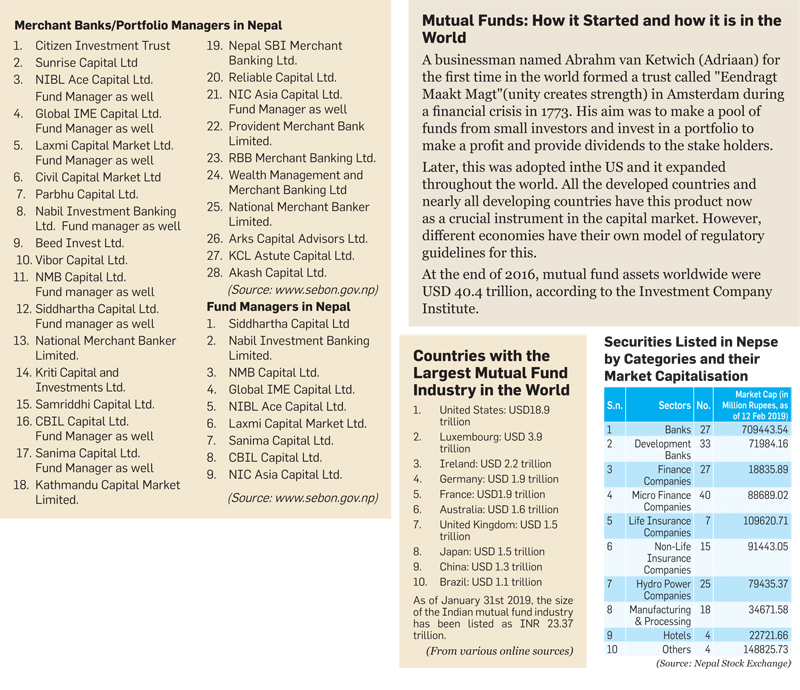

And the companies whose securities are listed in the stock exchange belong mainly to banking (commercial banks, development banks, finance companies and microfinance companies) and insurance, with a few companies from the hydropower sector. The number of companies, securities and market capitalisation of other sectors (such as services, manufacturing, hotels and trading) is very low. Mutual funds and their manager companies (merchant banks) too are listed in the stock exchange (they are grouped under the finance company category). However, their number and market capitalisation is very low. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard08%2818%29.jpg" style="width: 800px; height: 954px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Capital Market Expansion and Liquidity</strong></span></div>

<div style="text-align: justify;">

Till recently, trading in the Nepal Stock Exchange was accessible only to those who lived in Kathmandu valley or nearby as the brokers were located in the valley only. But the authorities are working to expand the market access. As a result, broker offices (Remote Work Stations) have been opened in some towns out of Kathmandu too. At present, Nepal Stock Exchange has installed a system through which any Nepali citizen, whether living within Nepal or anywhere in the world, can connect to the broker and buy or sell securities. The objective of introducing this electronic trading platform is to expand the number of investors in the securities. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Based on these circumstances, the number of people willing to invest in the stock market is sure to rise. This is likely to lead to higher frequency of price volatility in the securities market. These cycles need to be handled properly.That requires liquidity providers. Otherwise, a phase may come when the market itself may bleed dry. Mutual funds can play the role of such a liquidity provider. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

But the current regulatory provisions restrict mutual funds from playing this role. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Way Ahead: Bring New Types of Funds</strong></span></div>

<div style="text-align: justify;">

Then what can be done to improve the situation? </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

One is to start Open-ended Schemes. The mutual fund companies can do that under the existing regulatory provision. Let’s look at the regulatory provision: </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Open-ended Funds:</strong></span></div>

<div style="text-align: justify;">

The mutual fund regulation 2067, issued by Securities Exchange Board of Nepal (SEBON), defines in section 2(g) that "Open Ended Scheme" means a scheme which is operated without specifying any duration for redemption."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, open-end mutual funds must be willing to buy back ("redeem") their shares from their investors at the net asset value (NAV) computed that day based upon the prices of the securities owned by the fund. Most open-end funds also sell shares to the public every business day; these shares are priced at NAV.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This also means that there is no regulatory restriction in Nepal to launch open-ended mutual funds. The regulators should find out why the fund managers or trustees are not willing to start such schemes and bring out appropriate measures to encourage them to launch such schemes. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard09%2814%29.jpg" style="width: 800px; height: 352px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Closed-end Funds:</strong></span></div>

<div style="text-align: justify;">

The same mutual fund regulation 2067, in Section 2 (h) defines that a "Close Ended Scheme means a scheme which is operated specifying the period of maturity."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, closed-ended funds issue shares to the public only once, when they are created and issued through an initial public offering (IPO). Their shares are then listed for trading on the stock exchange. Investors who want to sell their shares can sell to another investor in the market; they cannot sell the shares back to the fund. The price that investors receive for their shares may be significantly different from NAV; it may be at a "premium" to NAV (i.e., higher than NAV) or, more commonly, at a "discount" to NAV (i.e., lower than NAV).</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

A number of such schemes are available right now in Nepal and their units can be bought and sold in the NEPSE. However, there is scope for improving such schemes as well. Such schemes can be tailored to suit the specific requirements of specific groups of investors based on the risk and return profile. For example, in Nepal the available schemes are named either “investment fund”, “equity fund” or “growth fund”, but there is none named as “debt fund” (that invests in debt instruments only), “money market fund” (that invests in money market instruments such as Treasury Bills only), “sector funds” (that invest in a particular specified sector, such as infrastructure, tourism, hydropower only), or “fixed income fund” (which promises a fixed income year after year). </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Unit Investment Trusts (UITs):</strong></span></div>

<div style="text-align: justify;">

This is another type of mutual fund that can be introduced in Nepal. This kind of scheme has not been defined properly in the regulation or guidelines from SEBON. So, none have been launched in Nepal. However, neither do the rules say that such schemes cannot be launched. UITs are issued to the general investors once they are created. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/12%284%29.jpg" style="width: 800px; height: 690px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>ETFs, REITs and Index Funds:</strong></span></div>

<div style="text-align: justify;">

Other new products that can be launched include Exchange Traded Funds (ETFs) and Real Estate Investment Trusts (REITs). They may be either open-ended funds or UITs, while index funds and other similar instruments may be Open-ended funds. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

REIT is defined as a company that owns, operates and or finances income-generating real estates. The idea of staring such an operation may be looked at with disdain at present because real estate investment is considered by the government and central bank authorities as “unproductive”. However, REITs are doing respectable business in other countries, including India. In Nepal too, the plan announced in the current year’s budget speech to start real estate brokerage firms and to make all real estate transactions only through such brokerages is likely to change the public attitude and create conducive environment for REITs. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Like UITs also, the ETFs, REITs and Index Funds are not yet operating in Nepal. Thus they will all be new to Nepal. However, they are popular in other countries. The introduction of REITs as UIT may not only help to regularise and organise the real estate market, they will also help to build the foundation for the infrastructure in this field for long term development. For investors in other countries where it is available, the main attraction of REITs has been their dividend yield. REIT dividends are secured by stable rents from long-term leases of the real estate. REIT shares are bought and sold on a stock exchange. Adding REITs to a diversified investment portfolio increases returns and reduces risks for both the fund manager and the investors.REITs raise money from a collection of investors and provide them with access to real estate. Publically traded REITs raise money for their portfolios by selling based on an exchange.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Open-ended funds, UITs, ETFs and REITs can be the tools for the stakeholders (fund managers and investors in the funds or unit holders) to manage their risk as per their respective risk appetite. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

After the Open-ended funds, UITs, ETFs and REITs, the next phase should see the introduction of Index Funds. It may not be as straightforward to start Index Funds soon as they are held in doubt, as such derivatives have been blamed for the 2008 global financial crisis. Though real estate derivatives too have been blamed for that crisis, REITs are not that complex derivatives. So they can be started easily.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

However, in a country where even the ‘right’ to renounce the ‘right to buy right shares’ issued by companies is not yet made tradable on the stock exchange, it still looks challenging to start even REITs. However, if the existing mutual fund managers and their trustees lobby with Security Market regulator SEBON and Financial Market Regulator Nepal Rastra Bank and they start serious dialogue on this, it is not impossible to start these funds.</div>

<div style="text-align: justify;">

</div>

',

'status' => true,

'publish_date' => null,

'created' => '2019-03-17 12:30:55',

'modified' => '2019-03-18 15:54:58',

'keywords' => '',

'description' => '',

'sortorder' => '2404',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '996',

'image' => '20190308092748_Clipboard01.jpg',

'sortorder' => '1544',

'published' => true,

'created' => '2019-03-06 14:49:26',

'modified' => '2019-03-08 09:27:48',

'title' => 'March 2019',

'publish_date' => '2019-03-01',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2449',

'magazine_issue_id' => '996',

'magazine_category_id' => '21',

'title' => 'Mutual Funds in Nepal : Way Ahead',

'image' => '20190317123055_Clipboard04.jpg',

'short_content' => 'The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. ',

'content' => '<div style="text-align: center;">

<span style="font-size:16px;"><em>Proper policies and strategies are required to develop the mutual fund market and cash in on the opportunities available in Nepal.</em></span></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<strong>--BY TEAM NEWBIZ</strong></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual Fund companies and the schemes they operate are running aground in Nepal. A new way forward has to be charted out for them. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

In reality, this is a pathetic state of affairs. Nepal has been historically slow in going ahead with the development of the capital market ecosystem (see box for some historical reference). The stock exchange was started in 1976. It took nearly two decades to start mutual funds and merchant banking companies that operate such funds. Though the number of merchant banks and thus the number of mutual funds in the market has now increased to 13, all the existing mutual fund schemes are close-ended. Though the market started in 1993 with both close-ended and open-ended mutual fund schemes, the new schemes of the open-ended category could not be launched. This has limited the options for the investors and stunted the growth potential of the merchant banks and thereby of the broader capital market. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard07%2813%29.jpg" style="width: 800px; height: 544px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Restrictive Regulation</strong></span></div>

<div style="text-align: justify;">

These fund managers (i.e. merchant banks) are required by the regulator to invest 90 % of the corpus on securities (stock) market – either in the Initial Public Offering (IPO) or from the secondary market. The rest has to be parked as deposits in commercial banks. Thus their Net Asset Value (NAV) totally depends on the performance of the securities market. If the securities market goes up or down, so does the NAV of the mutual funds. Therefore, while the stock market was going up, the mutual funds were doing well and gaining in their NAV and those who invested in these fund units were getting good dividends or capital gain. But in recent months, the market is going down and the NAV of the fund units that were issued at the face value of Rs. 10 has come down to around Rs. 8. This has started scaring the investors away from mutual funds. And the mutual funds are following two strategies. One, they are parking more funds than allowed in bank fixed deposits and paying penalties to the regulator. Second, they are buying more shares from the stock market at reduced prices and improving their average in the hopes that the market will bounce back sometime in the future. However, that is looking much like “Waiting for Godot”. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual funds create small-cap portfolios where small savers, those planning to enter the capital market as investors (both of them have low risk appetite), can invest and learn the ropes of the capital market. When this group of investors get scared away, the growth potential of the capital market gets constrained. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Lack of diversity in the securities listed in the Nepali stock market is one reason for this problem. Almost all the listed securities are shares (equity). Debt instruments (i.e. debentures) are very few and their trade is very rare, thus lacking liquidity. This lack of liquidity demotivates mutual funds from investing in debt instruments. This is one serious problem for the mutual funds when it comes to diversifying their portfolio. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

And the companies whose securities are listed in the stock exchange belong mainly to banking (commercial banks, development banks, finance companies and microfinance companies) and insurance, with a few companies from the hydropower sector. The number of companies, securities and market capitalisation of other sectors (such as services, manufacturing, hotels and trading) is very low. Mutual funds and their manager companies (merchant banks) too are listed in the stock exchange (they are grouped under the finance company category). However, their number and market capitalisation is very low. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard08%2818%29.jpg" style="width: 800px; height: 954px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Capital Market Expansion and Liquidity</strong></span></div>

<div style="text-align: justify;">

Till recently, trading in the Nepal Stock Exchange was accessible only to those who lived in Kathmandu valley or nearby as the brokers were located in the valley only. But the authorities are working to expand the market access. As a result, broker offices (Remote Work Stations) have been opened in some towns out of Kathmandu too. At present, Nepal Stock Exchange has installed a system through which any Nepali citizen, whether living within Nepal or anywhere in the world, can connect to the broker and buy or sell securities. The objective of introducing this electronic trading platform is to expand the number of investors in the securities. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Based on these circumstances, the number of people willing to invest in the stock market is sure to rise. This is likely to lead to higher frequency of price volatility in the securities market. These cycles need to be handled properly.That requires liquidity providers. Otherwise, a phase may come when the market itself may bleed dry. Mutual funds can play the role of such a liquidity provider. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

But the current regulatory provisions restrict mutual funds from playing this role. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Way Ahead: Bring New Types of Funds</strong></span></div>

<div style="text-align: justify;">

Then what can be done to improve the situation? </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

One is to start Open-ended Schemes. The mutual fund companies can do that under the existing regulatory provision. Let’s look at the regulatory provision: </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Open-ended Funds:</strong></span></div>

<div style="text-align: justify;">

The mutual fund regulation 2067, issued by Securities Exchange Board of Nepal (SEBON), defines in section 2(g) that "Open Ended Scheme" means a scheme which is operated without specifying any duration for redemption."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, open-end mutual funds must be willing to buy back ("redeem") their shares from their investors at the net asset value (NAV) computed that day based upon the prices of the securities owned by the fund. Most open-end funds also sell shares to the public every business day; these shares are priced at NAV.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This also means that there is no regulatory restriction in Nepal to launch open-ended mutual funds. The regulators should find out why the fund managers or trustees are not willing to start such schemes and bring out appropriate measures to encourage them to launch such schemes. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard09%2814%29.jpg" style="width: 800px; height: 352px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Closed-end Funds:</strong></span></div>

<div style="text-align: justify;">

The same mutual fund regulation 2067, in Section 2 (h) defines that a "Close Ended Scheme means a scheme which is operated specifying the period of maturity."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, closed-ended funds issue shares to the public only once, when they are created and issued through an initial public offering (IPO). Their shares are then listed for trading on the stock exchange. Investors who want to sell their shares can sell to another investor in the market; they cannot sell the shares back to the fund. The price that investors receive for their shares may be significantly different from NAV; it may be at a "premium" to NAV (i.e., higher than NAV) or, more commonly, at a "discount" to NAV (i.e., lower than NAV).</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

A number of such schemes are available right now in Nepal and their units can be bought and sold in the NEPSE. However, there is scope for improving such schemes as well. Such schemes can be tailored to suit the specific requirements of specific groups of investors based on the risk and return profile. For example, in Nepal the available schemes are named either “investment fund”, “equity fund” or “growth fund”, but there is none named as “debt fund” (that invests in debt instruments only), “money market fund” (that invests in money market instruments such as Treasury Bills only), “sector funds” (that invest in a particular specified sector, such as infrastructure, tourism, hydropower only), or “fixed income fund” (which promises a fixed income year after year). </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Unit Investment Trusts (UITs):</strong></span></div>

<div style="text-align: justify;">

This is another type of mutual fund that can be introduced in Nepal. This kind of scheme has not been defined properly in the regulation or guidelines from SEBON. So, none have been launched in Nepal. However, neither do the rules say that such schemes cannot be launched. UITs are issued to the general investors once they are created. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/12%284%29.jpg" style="width: 800px; height: 690px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>ETFs, REITs and Index Funds:</strong></span></div>

<div style="text-align: justify;">

Other new products that can be launched include Exchange Traded Funds (ETFs) and Real Estate Investment Trusts (REITs). They may be either open-ended funds or UITs, while index funds and other similar instruments may be Open-ended funds. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

REIT is defined as a company that owns, operates and or finances income-generating real estates. The idea of staring such an operation may be looked at with disdain at present because real estate investment is considered by the government and central bank authorities as “unproductive”. However, REITs are doing respectable business in other countries, including India. In Nepal too, the plan announced in the current year’s budget speech to start real estate brokerage firms and to make all real estate transactions only through such brokerages is likely to change the public attitude and create conducive environment for REITs. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Like UITs also, the ETFs, REITs and Index Funds are not yet operating in Nepal. Thus they will all be new to Nepal. However, they are popular in other countries. The introduction of REITs as UIT may not only help to regularise and organise the real estate market, they will also help to build the foundation for the infrastructure in this field for long term development. For investors in other countries where it is available, the main attraction of REITs has been their dividend yield. REIT dividends are secured by stable rents from long-term leases of the real estate. REIT shares are bought and sold on a stock exchange. Adding REITs to a diversified investment portfolio increases returns and reduces risks for both the fund manager and the investors.REITs raise money from a collection of investors and provide them with access to real estate. Publically traded REITs raise money for their portfolios by selling based on an exchange.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Open-ended funds, UITs, ETFs and REITs can be the tools for the stakeholders (fund managers and investors in the funds or unit holders) to manage their risk as per their respective risk appetite. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

After the Open-ended funds, UITs, ETFs and REITs, the next phase should see the introduction of Index Funds. It may not be as straightforward to start Index Funds soon as they are held in doubt, as such derivatives have been blamed for the 2008 global financial crisis. Though real estate derivatives too have been blamed for that crisis, REITs are not that complex derivatives. So they can be started easily.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

However, in a country where even the ‘right’ to renounce the ‘right to buy right shares’ issued by companies is not yet made tradable on the stock exchange, it still looks challenging to start even REITs. However, if the existing mutual fund managers and their trustees lobby with Security Market regulator SEBON and Financial Market Regulator Nepal Rastra Bank and they start serious dialogue on this, it is not impossible to start these funds.</div>

<div style="text-align: justify;">

</div>

',

'status' => true,

'publish_date' => null,

'created' => '2019-03-17 12:30:55',

'modified' => '2019-03-18 15:54:58',

'keywords' => '',

'description' => '',

'sortorder' => '2404',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '996',

'image' => '20190308092748_Clipboard01.jpg',

'sortorder' => '1544',

'published' => true,

'created' => '2019-03-06 14:49:26',

'modified' => '2019-03-08 09:27:48',

'title' => 'March 2019',

'publish_date' => '2019-03-01',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2449',

'hit' => '7947'

)

)

)

$current_user = null

$logged_in = false

$user = null

include - APP/View/MagazineArticles/view.ctp, line 54

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Trying to access array offset on value of type null [APP/View/MagazineArticles/view.ctp, line 54]

$user = $this->Session->read('Auth.User');

//find the group of logged user

$groupId = $user['Group']['id'];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2449',

'magazine_issue_id' => '996',

'magazine_category_id' => '21',

'title' => 'Mutual Funds in Nepal : Way Ahead',

'image' => '20190317123055_Clipboard04.jpg',

'short_content' => 'The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. ',

'content' => '<div style="text-align: center;">

<span style="font-size:16px;"><em>Proper policies and strategies are required to develop the mutual fund market and cash in on the opportunities available in Nepal.</em></span></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<strong>--BY TEAM NEWBIZ</strong></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual Fund companies and the schemes they operate are running aground in Nepal. A new way forward has to be charted out for them. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

In reality, this is a pathetic state of affairs. Nepal has been historically slow in going ahead with the development of the capital market ecosystem (see box for some historical reference). The stock exchange was started in 1976. It took nearly two decades to start mutual funds and merchant banking companies that operate such funds. Though the number of merchant banks and thus the number of mutual funds in the market has now increased to 13, all the existing mutual fund schemes are close-ended. Though the market started in 1993 with both close-ended and open-ended mutual fund schemes, the new schemes of the open-ended category could not be launched. This has limited the options for the investors and stunted the growth potential of the merchant banks and thereby of the broader capital market. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard07%2813%29.jpg" style="width: 800px; height: 544px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Restrictive Regulation</strong></span></div>

<div style="text-align: justify;">

These fund managers (i.e. merchant banks) are required by the regulator to invest 90 % of the corpus on securities (stock) market – either in the Initial Public Offering (IPO) or from the secondary market. The rest has to be parked as deposits in commercial banks. Thus their Net Asset Value (NAV) totally depends on the performance of the securities market. If the securities market goes up or down, so does the NAV of the mutual funds. Therefore, while the stock market was going up, the mutual funds were doing well and gaining in their NAV and those who invested in these fund units were getting good dividends or capital gain. But in recent months, the market is going down and the NAV of the fund units that were issued at the face value of Rs. 10 has come down to around Rs. 8. This has started scaring the investors away from mutual funds. And the mutual funds are following two strategies. One, they are parking more funds than allowed in bank fixed deposits and paying penalties to the regulator. Second, they are buying more shares from the stock market at reduced prices and improving their average in the hopes that the market will bounce back sometime in the future. However, that is looking much like “Waiting for Godot”. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual funds create small-cap portfolios where small savers, those planning to enter the capital market as investors (both of them have low risk appetite), can invest and learn the ropes of the capital market. When this group of investors get scared away, the growth potential of the capital market gets constrained. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Lack of diversity in the securities listed in the Nepali stock market is one reason for this problem. Almost all the listed securities are shares (equity). Debt instruments (i.e. debentures) are very few and their trade is very rare, thus lacking liquidity. This lack of liquidity demotivates mutual funds from investing in debt instruments. This is one serious problem for the mutual funds when it comes to diversifying their portfolio. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

And the companies whose securities are listed in the stock exchange belong mainly to banking (commercial banks, development banks, finance companies and microfinance companies) and insurance, with a few companies from the hydropower sector. The number of companies, securities and market capitalisation of other sectors (such as services, manufacturing, hotels and trading) is very low. Mutual funds and their manager companies (merchant banks) too are listed in the stock exchange (they are grouped under the finance company category). However, their number and market capitalisation is very low. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard08%2818%29.jpg" style="width: 800px; height: 954px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Capital Market Expansion and Liquidity</strong></span></div>

<div style="text-align: justify;">

Till recently, trading in the Nepal Stock Exchange was accessible only to those who lived in Kathmandu valley or nearby as the brokers were located in the valley only. But the authorities are working to expand the market access. As a result, broker offices (Remote Work Stations) have been opened in some towns out of Kathmandu too. At present, Nepal Stock Exchange has installed a system through which any Nepali citizen, whether living within Nepal or anywhere in the world, can connect to the broker and buy or sell securities. The objective of introducing this electronic trading platform is to expand the number of investors in the securities. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Based on these circumstances, the number of people willing to invest in the stock market is sure to rise. This is likely to lead to higher frequency of price volatility in the securities market. These cycles need to be handled properly.That requires liquidity providers. Otherwise, a phase may come when the market itself may bleed dry. Mutual funds can play the role of such a liquidity provider. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

But the current regulatory provisions restrict mutual funds from playing this role. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Way Ahead: Bring New Types of Funds</strong></span></div>

<div style="text-align: justify;">

Then what can be done to improve the situation? </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

One is to start Open-ended Schemes. The mutual fund companies can do that under the existing regulatory provision. Let’s look at the regulatory provision: </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Open-ended Funds:</strong></span></div>

<div style="text-align: justify;">

The mutual fund regulation 2067, issued by Securities Exchange Board of Nepal (SEBON), defines in section 2(g) that "Open Ended Scheme" means a scheme which is operated without specifying any duration for redemption."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, open-end mutual funds must be willing to buy back ("redeem") their shares from their investors at the net asset value (NAV) computed that day based upon the prices of the securities owned by the fund. Most open-end funds also sell shares to the public every business day; these shares are priced at NAV.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This also means that there is no regulatory restriction in Nepal to launch open-ended mutual funds. The regulators should find out why the fund managers or trustees are not willing to start such schemes and bring out appropriate measures to encourage them to launch such schemes. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard09%2814%29.jpg" style="width: 800px; height: 352px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Closed-end Funds:</strong></span></div>

<div style="text-align: justify;">

The same mutual fund regulation 2067, in Section 2 (h) defines that a "Close Ended Scheme means a scheme which is operated specifying the period of maturity."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, closed-ended funds issue shares to the public only once, when they are created and issued through an initial public offering (IPO). Their shares are then listed for trading on the stock exchange. Investors who want to sell their shares can sell to another investor in the market; they cannot sell the shares back to the fund. The price that investors receive for their shares may be significantly different from NAV; it may be at a "premium" to NAV (i.e., higher than NAV) or, more commonly, at a "discount" to NAV (i.e., lower than NAV).</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

A number of such schemes are available right now in Nepal and their units can be bought and sold in the NEPSE. However, there is scope for improving such schemes as well. Such schemes can be tailored to suit the specific requirements of specific groups of investors based on the risk and return profile. For example, in Nepal the available schemes are named either “investment fund”, “equity fund” or “growth fund”, but there is none named as “debt fund” (that invests in debt instruments only), “money market fund” (that invests in money market instruments such as Treasury Bills only), “sector funds” (that invest in a particular specified sector, such as infrastructure, tourism, hydropower only), or “fixed income fund” (which promises a fixed income year after year). </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Unit Investment Trusts (UITs):</strong></span></div>

<div style="text-align: justify;">

This is another type of mutual fund that can be introduced in Nepal. This kind of scheme has not been defined properly in the regulation or guidelines from SEBON. So, none have been launched in Nepal. However, neither do the rules say that such schemes cannot be launched. UITs are issued to the general investors once they are created. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/12%284%29.jpg" style="width: 800px; height: 690px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>ETFs, REITs and Index Funds:</strong></span></div>

<div style="text-align: justify;">

Other new products that can be launched include Exchange Traded Funds (ETFs) and Real Estate Investment Trusts (REITs). They may be either open-ended funds or UITs, while index funds and other similar instruments may be Open-ended funds. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

REIT is defined as a company that owns, operates and or finances income-generating real estates. The idea of staring such an operation may be looked at with disdain at present because real estate investment is considered by the government and central bank authorities as “unproductive”. However, REITs are doing respectable business in other countries, including India. In Nepal too, the plan announced in the current year’s budget speech to start real estate brokerage firms and to make all real estate transactions only through such brokerages is likely to change the public attitude and create conducive environment for REITs. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Like UITs also, the ETFs, REITs and Index Funds are not yet operating in Nepal. Thus they will all be new to Nepal. However, they are popular in other countries. The introduction of REITs as UIT may not only help to regularise and organise the real estate market, they will also help to build the foundation for the infrastructure in this field for long term development. For investors in other countries where it is available, the main attraction of REITs has been their dividend yield. REIT dividends are secured by stable rents from long-term leases of the real estate. REIT shares are bought and sold on a stock exchange. Adding REITs to a diversified investment portfolio increases returns and reduces risks for both the fund manager and the investors.REITs raise money from a collection of investors and provide them with access to real estate. Publically traded REITs raise money for their portfolios by selling based on an exchange.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Open-ended funds, UITs, ETFs and REITs can be the tools for the stakeholders (fund managers and investors in the funds or unit holders) to manage their risk as per their respective risk appetite. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

After the Open-ended funds, UITs, ETFs and REITs, the next phase should see the introduction of Index Funds. It may not be as straightforward to start Index Funds soon as they are held in doubt, as such derivatives have been blamed for the 2008 global financial crisis. Though real estate derivatives too have been blamed for that crisis, REITs are not that complex derivatives. So they can be started easily.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

However, in a country where even the ‘right’ to renounce the ‘right to buy right shares’ issued by companies is not yet made tradable on the stock exchange, it still looks challenging to start even REITs. However, if the existing mutual fund managers and their trustees lobby with Security Market regulator SEBON and Financial Market Regulator Nepal Rastra Bank and they start serious dialogue on this, it is not impossible to start these funds.</div>

<div style="text-align: justify;">

</div>

',

'status' => true,

'publish_date' => null,

'created' => '2019-03-17 12:30:55',

'modified' => '2019-03-18 15:54:58',

'keywords' => '',

'description' => '',

'sortorder' => '2404',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '996',

'image' => '20190308092748_Clipboard01.jpg',

'sortorder' => '1544',

'published' => true,

'created' => '2019-03-06 14:49:26',

'modified' => '2019-03-08 09:27:48',

'title' => 'March 2019',

'publish_date' => '2019-03-01',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

[maximum depth reached]

)

)

),

'current_user' => null,

'logged_in' => false

)

$magazineArticle = array(

'MagazineArticle' => array(

'id' => '2449',

'magazine_issue_id' => '996',

'magazine_category_id' => '21',

'title' => 'Mutual Funds in Nepal : Way Ahead',

'image' => '20190317123055_Clipboard04.jpg',

'short_content' => 'The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. ',

'content' => '<div style="text-align: center;">

<span style="font-size:16px;"><em>Proper policies and strategies are required to develop the mutual fund market and cash in on the opportunities available in Nepal.</em></span></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<strong>--BY TEAM NEWBIZ</strong></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual Fund companies and the schemes they operate are running aground in Nepal. A new way forward has to be charted out for them. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

In reality, this is a pathetic state of affairs. Nepal has been historically slow in going ahead with the development of the capital market ecosystem (see box for some historical reference). The stock exchange was started in 1976. It took nearly two decades to start mutual funds and merchant banking companies that operate such funds. Though the number of merchant banks and thus the number of mutual funds in the market has now increased to 13, all the existing mutual fund schemes are close-ended. Though the market started in 1993 with both close-ended and open-ended mutual fund schemes, the new schemes of the open-ended category could not be launched. This has limited the options for the investors and stunted the growth potential of the merchant banks and thereby of the broader capital market. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard07%2813%29.jpg" style="width: 800px; height: 544px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Restrictive Regulation</strong></span></div>

<div style="text-align: justify;">

These fund managers (i.e. merchant banks) are required by the regulator to invest 90 % of the corpus on securities (stock) market – either in the Initial Public Offering (IPO) or from the secondary market. The rest has to be parked as deposits in commercial banks. Thus their Net Asset Value (NAV) totally depends on the performance of the securities market. If the securities market goes up or down, so does the NAV of the mutual funds. Therefore, while the stock market was going up, the mutual funds were doing well and gaining in their NAV and those who invested in these fund units were getting good dividends or capital gain. But in recent months, the market is going down and the NAV of the fund units that were issued at the face value of Rs. 10 has come down to around Rs. 8. This has started scaring the investors away from mutual funds. And the mutual funds are following two strategies. One, they are parking more funds than allowed in bank fixed deposits and paying penalties to the regulator. Second, they are buying more shares from the stock market at reduced prices and improving their average in the hopes that the market will bounce back sometime in the future. However, that is looking much like “Waiting for Godot”. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual funds create small-cap portfolios where small savers, those planning to enter the capital market as investors (both of them have low risk appetite), can invest and learn the ropes of the capital market. When this group of investors get scared away, the growth potential of the capital market gets constrained. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Lack of diversity in the securities listed in the Nepali stock market is one reason for this problem. Almost all the listed securities are shares (equity). Debt instruments (i.e. debentures) are very few and their trade is very rare, thus lacking liquidity. This lack of liquidity demotivates mutual funds from investing in debt instruments. This is one serious problem for the mutual funds when it comes to diversifying their portfolio. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

And the companies whose securities are listed in the stock exchange belong mainly to banking (commercial banks, development banks, finance companies and microfinance companies) and insurance, with a few companies from the hydropower sector. The number of companies, securities and market capitalisation of other sectors (such as services, manufacturing, hotels and trading) is very low. Mutual funds and their manager companies (merchant banks) too are listed in the stock exchange (they are grouped under the finance company category). However, their number and market capitalisation is very low. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard08%2818%29.jpg" style="width: 800px; height: 954px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Capital Market Expansion and Liquidity</strong></span></div>

<div style="text-align: justify;">

Till recently, trading in the Nepal Stock Exchange was accessible only to those who lived in Kathmandu valley or nearby as the brokers were located in the valley only. But the authorities are working to expand the market access. As a result, broker offices (Remote Work Stations) have been opened in some towns out of Kathmandu too. At present, Nepal Stock Exchange has installed a system through which any Nepali citizen, whether living within Nepal or anywhere in the world, can connect to the broker and buy or sell securities. The objective of introducing this electronic trading platform is to expand the number of investors in the securities. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Based on these circumstances, the number of people willing to invest in the stock market is sure to rise. This is likely to lead to higher frequency of price volatility in the securities market. These cycles need to be handled properly.That requires liquidity providers. Otherwise, a phase may come when the market itself may bleed dry. Mutual funds can play the role of such a liquidity provider. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

But the current regulatory provisions restrict mutual funds from playing this role. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Way Ahead: Bring New Types of Funds</strong></span></div>

<div style="text-align: justify;">

Then what can be done to improve the situation? </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

One is to start Open-ended Schemes. The mutual fund companies can do that under the existing regulatory provision. Let’s look at the regulatory provision: </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Open-ended Funds:</strong></span></div>

<div style="text-align: justify;">

The mutual fund regulation 2067, issued by Securities Exchange Board of Nepal (SEBON), defines in section 2(g) that "Open Ended Scheme" means a scheme which is operated without specifying any duration for redemption."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, open-end mutual funds must be willing to buy back ("redeem") their shares from their investors at the net asset value (NAV) computed that day based upon the prices of the securities owned by the fund. Most open-end funds also sell shares to the public every business day; these shares are priced at NAV.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This also means that there is no regulatory restriction in Nepal to launch open-ended mutual funds. The regulators should find out why the fund managers or trustees are not willing to start such schemes and bring out appropriate measures to encourage them to launch such schemes. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard09%2814%29.jpg" style="width: 800px; height: 352px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Closed-end Funds:</strong></span></div>

<div style="text-align: justify;">

The same mutual fund regulation 2067, in Section 2 (h) defines that a "Close Ended Scheme means a scheme which is operated specifying the period of maturity."</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

This means, closed-ended funds issue shares to the public only once, when they are created and issued through an initial public offering (IPO). Their shares are then listed for trading on the stock exchange. Investors who want to sell their shares can sell to another investor in the market; they cannot sell the shares back to the fund. The price that investors receive for their shares may be significantly different from NAV; it may be at a "premium" to NAV (i.e., higher than NAV) or, more commonly, at a "discount" to NAV (i.e., lower than NAV).</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

A number of such schemes are available right now in Nepal and their units can be bought and sold in the NEPSE. However, there is scope for improving such schemes as well. Such schemes can be tailored to suit the specific requirements of specific groups of investors based on the risk and return profile. For example, in Nepal the available schemes are named either “investment fund”, “equity fund” or “growth fund”, but there is none named as “debt fund” (that invests in debt instruments only), “money market fund” (that invests in money market instruments such as Treasury Bills only), “sector funds” (that invest in a particular specified sector, such as infrastructure, tourism, hydropower only), or “fixed income fund” (which promises a fixed income year after year). </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Unit Investment Trusts (UITs):</strong></span></div>

<div style="text-align: justify;">

This is another type of mutual fund that can be introduced in Nepal. This kind of scheme has not been defined properly in the regulation or guidelines from SEBON. So, none have been launched in Nepal. However, neither do the rules say that such schemes cannot be launched. UITs are issued to the general investors once they are created. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/12%284%29.jpg" style="width: 800px; height: 690px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>ETFs, REITs and Index Funds:</strong></span></div>

<div style="text-align: justify;">

Other new products that can be launched include Exchange Traded Funds (ETFs) and Real Estate Investment Trusts (REITs). They may be either open-ended funds or UITs, while index funds and other similar instruments may be Open-ended funds. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

REIT is defined as a company that owns, operates and or finances income-generating real estates. The idea of staring such an operation may be looked at with disdain at present because real estate investment is considered by the government and central bank authorities as “unproductive”. However, REITs are doing respectable business in other countries, including India. In Nepal too, the plan announced in the current year’s budget speech to start real estate brokerage firms and to make all real estate transactions only through such brokerages is likely to change the public attitude and create conducive environment for REITs. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Like UITs also, the ETFs, REITs and Index Funds are not yet operating in Nepal. Thus they will all be new to Nepal. However, they are popular in other countries. The introduction of REITs as UIT may not only help to regularise and organise the real estate market, they will also help to build the foundation for the infrastructure in this field for long term development. For investors in other countries where it is available, the main attraction of REITs has been their dividend yield. REIT dividends are secured by stable rents from long-term leases of the real estate. REIT shares are bought and sold on a stock exchange. Adding REITs to a diversified investment portfolio increases returns and reduces risks for both the fund manager and the investors.REITs raise money from a collection of investors and provide them with access to real estate. Publically traded REITs raise money for their portfolios by selling based on an exchange.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Open-ended funds, UITs, ETFs and REITs can be the tools for the stakeholders (fund managers and investors in the funds or unit holders) to manage their risk as per their respective risk appetite. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

After the Open-ended funds, UITs, ETFs and REITs, the next phase should see the introduction of Index Funds. It may not be as straightforward to start Index Funds soon as they are held in doubt, as such derivatives have been blamed for the 2008 global financial crisis. Though real estate derivatives too have been blamed for that crisis, REITs are not that complex derivatives. So they can be started easily.</div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

However, in a country where even the ‘right’ to renounce the ‘right to buy right shares’ issued by companies is not yet made tradable on the stock exchange, it still looks challenging to start even REITs. However, if the existing mutual fund managers and their trustees lobby with Security Market regulator SEBON and Financial Market Regulator Nepal Rastra Bank and they start serious dialogue on this, it is not impossible to start these funds.</div>

<div style="text-align: justify;">

</div>

',

'status' => true,

'publish_date' => null,

'created' => '2019-03-17 12:30:55',

'modified' => '2019-03-18 15:54:58',

'keywords' => '',

'description' => '',

'sortorder' => '2404',

'feature_article' => true,

'user_id' => '11',

'image1' => null,

'image2' => null,

'image3' => null,

'image4' => null

),

'MagazineIssue' => array(

'id' => '996',

'image' => '20190308092748_Clipboard01.jpg',

'sortorder' => '1544',

'published' => true,

'created' => '2019-03-06 14:49:26',

'modified' => '2019-03-08 09:27:48',

'title' => 'March 2019',

'publish_date' => '2019-03-01',

'parent_id' => '0',

'homepage' => true,

'user_id' => '11'

),

'MagazineCategory' => array(

'id' => '21',

'title' => 'Cover Story',

'sortorder' => '532',

'status' => true,

'created' => '0000-00-00 00:00:00',

'homepage' => true,

'modified' => '2017-05-03 14:57:12'

),

'User' => array(

'password' => '*****',

'id' => '11',

'user_detail_id' => '0',

'group_id' => '24',

'username' => 'nsingha@abhiyan.com.np',

'name' => '',

'email' => 'nsingha@abhiyan.com.np',

'address' => '',

'gender' => '',

'access' => '1',

'phone' => '',

'access_type' => '0',

'activated' => false,

'sortorder' => '0',

'published' => '0',

'created' => '2015-04-08 13:22:59',

'last_login' => '2023-04-16 09:29:47',

'ip' => '172.69.77.43'

),

'MagazineArticleComment' => array(),

'MagazineView' => array(

(int) 0 => array(

'magazine_article_id' => '2449',

'hit' => '7947'

)

)

)

$current_user = null

$logged_in = false

$user = null

include - APP/View/MagazineArticles/view.ctp, line 54

View::_evaluate() - CORE/Cake/View/View.php, line 971

View::_render() - CORE/Cake/View/View.php, line 933

View::render() - CORE/Cake/View/View.php, line 473

Controller::render() - CORE/Cake/Controller/Controller.php, line 968

Dispatcher::_invoke() - CORE/Cake/Routing/Dispatcher.php, line 200

Dispatcher::dispatch() - CORE/Cake/Routing/Dispatcher.php, line 167

[main] - APP/webroot/index.php, line 117

Notice (8): Trying to access array offset on value of type null [APP/View/MagazineArticles/view.ctp, line 55]

//find the group of logged user

$groupId = $user['Group']['id'];

$user_id=$user["id"];

$viewFile = '/var/www/html/newbusinessage.com/app/View/MagazineArticles/view.ctp'

$dataForView = array(

'magazineArticle' => array(

'MagazineArticle' => array(

'id' => '2449',

'magazine_issue_id' => '996',

'magazine_category_id' => '21',

'title' => 'Mutual Funds in Nepal : Way Ahead',

'image' => '20190317123055_Clipboard04.jpg',

'short_content' => 'The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. ',

'content' => '<div style="text-align: center;">

<span style="font-size:16px;"><em>Proper policies and strategies are required to develop the mutual fund market and cash in on the opportunities available in Nepal.</em></span></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<strong>--BY TEAM NEWBIZ</strong></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual Fund companies and the schemes they operate are running aground in Nepal. A new way forward has to be charted out for them. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

The development or growth or expansion of the capital market in Nepal has been talked about a lot. However, these discussions have made little real impact. Thus, the Nepali capital market is operating in an ecosystem where many components are entirely absent. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

In reality, this is a pathetic state of affairs. Nepal has been historically slow in going ahead with the development of the capital market ecosystem (see box for some historical reference). The stock exchange was started in 1976. It took nearly two decades to start mutual funds and merchant banking companies that operate such funds. Though the number of merchant banks and thus the number of mutual funds in the market has now increased to 13, all the existing mutual fund schemes are close-ended. Though the market started in 1993 with both close-ended and open-ended mutual fund schemes, the new schemes of the open-ended category could not be launched. This has limited the options for the investors and stunted the growth potential of the merchant banks and thereby of the broader capital market. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard07%2813%29.jpg" style="width: 800px; height: 544px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Restrictive Regulation</strong></span></div>

<div style="text-align: justify;">

These fund managers (i.e. merchant banks) are required by the regulator to invest 90 % of the corpus on securities (stock) market – either in the Initial Public Offering (IPO) or from the secondary market. The rest has to be parked as deposits in commercial banks. Thus their Net Asset Value (NAV) totally depends on the performance of the securities market. If the securities market goes up or down, so does the NAV of the mutual funds. Therefore, while the stock market was going up, the mutual funds were doing well and gaining in their NAV and those who invested in these fund units were getting good dividends or capital gain. But in recent months, the market is going down and the NAV of the fund units that were issued at the face value of Rs. 10 has come down to around Rs. 8. This has started scaring the investors away from mutual funds. And the mutual funds are following two strategies. One, they are parking more funds than allowed in bank fixed deposits and paying penalties to the regulator. Second, they are buying more shares from the stock market at reduced prices and improving their average in the hopes that the market will bounce back sometime in the future. However, that is looking much like “Waiting for Godot”. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Mutual funds create small-cap portfolios where small savers, those planning to enter the capital market as investors (both of them have low risk appetite), can invest and learn the ropes of the capital market. When this group of investors get scared away, the growth potential of the capital market gets constrained. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

Lack of diversity in the securities listed in the Nepali stock market is one reason for this problem. Almost all the listed securities are shares (equity). Debt instruments (i.e. debentures) are very few and their trade is very rare, thus lacking liquidity. This lack of liquidity demotivates mutual funds from investing in debt instruments. This is one serious problem for the mutual funds when it comes to diversifying their portfolio. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

And the companies whose securities are listed in the stock exchange belong mainly to banking (commercial banks, development banks, finance companies and microfinance companies) and insurance, with a few companies from the hydropower sector. The number of companies, securities and market capitalisation of other sectors (such as services, manufacturing, hotels and trading) is very low. Mutual funds and their manager companies (merchant banks) too are listed in the stock exchange (they are grouped under the finance company category). However, their number and market capitalisation is very low. </div>

<div style="text-align: justify;">

</div>

<div style="text-align: center;">

<img alt="" src="/app/webroot/userfiles/images/Clipboard08%2818%29.jpg" style="width: 800px; height: 954px;" /></div>

<div style="text-align: justify;">

</div>

<div style="text-align: justify;">

<span style="font-size:16px;"><strong>Capital Market Expansion and Liquidity</strong></span></div>

<div style="text-align: justify;">